In this post, I lay out some problems that I have encountered in attempting to reconcile what it will mean for a D-SIB ADI to be “Unquestionably Strong” under the proposed new framework that APRA outlined in its December 2020 Discussion Paper (“A more flexible and resilient capital framework for ADIs”). Spoiler alert – I think the capital buffers adding up to a 10.5% CET1 prudential requirement may need to be recalibrated once all of the proposed changes to risk weights are tied down. I also include some questions regarding the impact of the RBNZ’s requirement for substantially higher capital requirements for NZ domiciled banks.

The backstory

The idea that Australian Authorised Deposit Taking Institutions (“ADIs” but more commonly referred to as “banks”) needed to be “Unquestionably Strong” originated in a recommendation of the Australian Financial System Inquiry (2014) based on the rationale that Australian ADIs should both be and, equally importantly, be perceived to be more resilient than the international peers with which they compete for funding in the international capital markets.In July 2017, APRA translated the FSI recommendation into practical guidance in an announcementsupported by a longer information paper.

For most people, this all condensed into a very simple message, the systemically important Australian ADIs needed to maintain a Common Equity Tier 1 (CET1) ratio of at least 10.5%. The smaller ADIs have their own Unquestionably Strong benchmark but most of the public scrutiny seems to have focussed on the larger systemically important ADIs.

In the background, an equally important discussion has been playing out regarding the extent to which the Unquestionably Strong framework should take account of the “comparability” and “transparency” of that measure of strength and the ways in which “flexibility” and “resilience” could be added to the mix. This discussion kicked off in earnest with a March 2018 APRA discussion paper (which I covered here) and has come to a conclusion with the December 2020 release of the APRA Discussion Paper explored in the post above.

December 2020 – “Unquestionably Strong” meets “A more flexible and resilient capital framework for ADIs”

I have written a couple of posts on APRA’s December 2020 Discussion Paper but have thus far focussed on the details of the proposed changes to risk weights and capital buffers (here, here and here). This was partly because there was a lot to digest in these proposals but also because I simply found the discussion of how the proposed new framework reconciled to the Unquestionably Strong benchmark to be a bit confusing.

What follows is my current understanding of what the DP says and where we are headed.

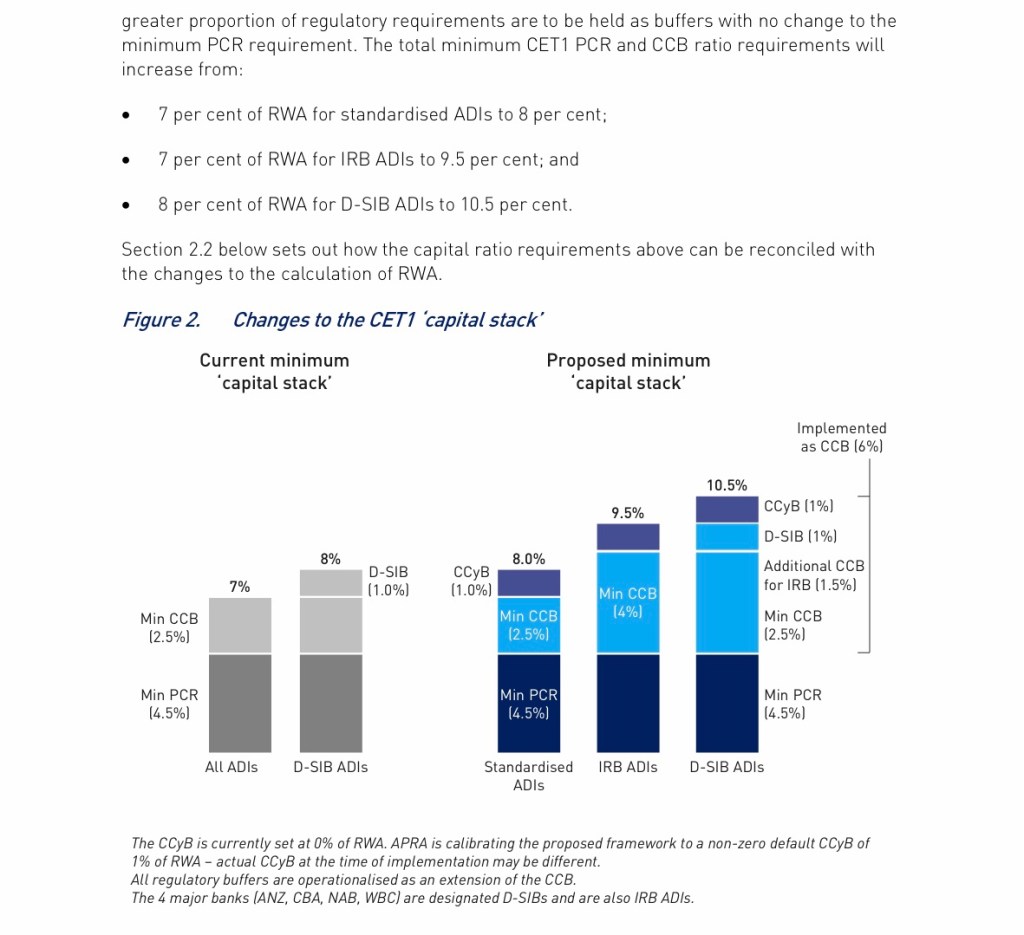

On one level, the answer is quite simple – Exhibit A from the Discussion Paper (page 17) …

- For systemically important ADI (D-SIB ADIs), the Unquestionably Strong 10.5% CET1 benchmark will be enshrined in a series of expanded capital buffers that will come into force on 1 January 2023 and add up to 10.5%.

- However, we also know that APRA has at the same time outlined a range of enhancements to risk weights that are expected to have the effect of reducing aggregate Risk Weighted Assets and thereby result in higher capital adequacy ratios.

- APRA has also emphasised that the net impact of the changes is intended to be capital neutral; i.e. any D-SIB ADI that meets the Unquestionably Strong benchmark now (i.e. that had a CET1 ratio of at least 10.5% under the current framework) will be Unquestionably Strong under the new framework

- However this implies that the expected increase in reported CET1 under the new framework will not represent surplus capital so it looks like Unquestionably Strong will require a CET1 ratio higher than 10.5% once the new framework comes into place.

The only way I can reconcile this is to assume that APRA will be revisiting the calibration of the proposed increased capital buffers once it gets a better handle on how much capital ratios will increase in response to the changes it makes to bring Australian capital ratios closer to those calculated by international peers under the Basel minimum requirements. If this was spelled out in the Discussion Paper I missed it.

What about the impact of RBNZ requiring more capital to be held in New Zealand?

Running alongside the big picture issues summarised above (Unquestionably Strong, Transparency, Comparability, Flexibility, Resilience”, APRA has also been looking at how it should respond to the issues posed by the RBNZ policy applying substantial increases to the capital requirements for banks operating in NZ. I wrote two post on this issue (see here and here) that make the following points

- To understand what is going on here you need to understand the difference between “Level 1” and Level 2” Capital Adequacy (part of the price of entry to this discussion is understanding more APRA jargon)

- The increased share of the group capital resources required to be maintained in NZ will not have any impact on the Level 2 capital adequacy ratios that are the ones most commonly cited when discussing Australian ADI capital strength

- In theory, maintaining the status quo share of group capital resources maintained in Australia would require some increase in the Level 2 CET1 ratio (i.e. the one that is used to express the Unquestionably Strong benchmark)

- In practice, the extent to which the Level 2 benchmark is impacted depends on the maternity of the NZ business so it may be that there is nothing to see here

- It is hard to tell however partly because there is not a lot of disclosure on the details of the Level 1 capital adequacy ratios (at least not a lot that I could find) and partly because the Level 1 capital measure is (to my mind) not an especially reliable (or indeed intuitive) measure of the capital strength

Summing up

- There is I think a general consensus that the Australian D-SIB ADIs all currently exceed the requirements of what it means to be Unquestionably Strong under the current capital adequacy framework

- This implies that they have surplus capital that may potentially be returned to shareholders

- APRA has laid out what I believe to be pretty sensible and useful enhancements to that framework (the expanded and explicitly more flexible capital buffers in particular)

- These changes have however (for me at least) made it less clear what it will mean for an ADI to be Unquestionably Strong post 1 January 2023 when the proposed changes to Risk Weighted Assets come into effect

Any and all contributions to reducing my ignorance and confusion will be gratefully accepted – let me know what I am missing

Tony – From the Outside