Chapter III of the BIS’s 2021 Annual Economic Report titled “CBDCs: an opportunity for the monetary system” examines how, in the BIS’s words, CBDCs “… can contribute to an open, safe and competitive monetary system that supports innovation and serves the public interest”. Unless otherwise noted, all quotes below are from the BIS report.

The BIS highlights four key takeaways:

– Central bank digital currencies (CBDCs) offer in digital form the unique advantages of central bank money: settlement finality, liquidity and integrity. They are an advanced representation of money for the digital economy.

– Digital money should be designed with the public interest in mind. Like the latest generation of instant retail payment systems, retail CBDCs could ensure open payment platforms and a competitive level playing field that is conducive to innovation.

– The ultimate benefits of adopting a new payment technology will depend on the competitive structure of the underlying payment system and data governance arrangements. The same technology that can encourage a virtuous circle of greater access, lower costs and better services might equally induce a vicious circle of data silos, market power and anti-competitive practices. CBDCs and open platforms are the most conducive to a virtuous circle.

– CBDCs built on digital identification could improve cross-border payments, and limit the risks of currency substitution. Multi-CBDC arrangements could surmount the hurdles of sharing digital IDs across borders, but will require international cooperation.

Introduction

The BIS notes that a digital economy obviously requires a digital currency but a digital economy also brings new challenges associated with the networks effects that concentrate market power in “big tech” companies and the personal data that the digital economy generates…

Digital innovation has wrought far-reaching changes in all sectors of the economy. Alongside a broader trend towards greater digitalisation, a wave of innovation in consumer payments has placed money and payment services at the vanguard of this development. An essential by-product of the digital economy is the huge volume of personal data that are collected and processed as an input into business activity. This raises issues of data governance, consumer protection and anti-competitive practices arising from data silos.

The paper seeks to make the case for CBDCs having an important place in the digital economy but we need to clarify what distinguishes CBDC from existing forms of digital money (i.e. central bank reserve accounts and customer bank deposits with commercial banks)…

CBDCs are a form of digital money, denominated in the national unit of account, which is a direct liability of the central bank. CBDCs can be designed for use either among financial intermediaries only (ie wholesale CBDCs), or by the wider economy (ie retail CBDCs).

The distinguishing feature of a CBDC is that it is a “direct liability” of the central bank. It has been argued elsewhere that a digital currency fully backed (maybe even over-collateralised) by reserves held in a central bank account would be safe enough but the BIS begs to differ. The “unique advantages” of central bank money (i.e. “settlement finality, liquidity and integrity”) in its view require that the digital instrument be a direct liability of the central bank with no intermediary. A “narrow bank” might be argued to be safer than the conventional “fractional reserve” banking model that currently provides the bulk of the digital currency in use but it is not, in the BIS perspective, good enough.

It is worth contrasting the BIS approach with an alternative perspective put forward by Randall Quarles, a member of the Federal Reserve Board of Governors and Vice Chair for Supervision who is open (at least in principle) to alternative forms of digital money being developed by private sector actors

When our concerns have been addressed, we should be saying yes to these products, rather than straining to find ways to say no. Indeed, the combination of imminent improvements in the existing payments system such as various instant payments initiatives combined with the cross-border efficiency of properly structured stablecoins could well make superfluous any effort to develop a CBDC.

Speech “Parachute Pants and Central Bank Money” by Vice Chair for Supervision Quarles, Federal Reserve Board of Governors at the Annual Utah Bankers Association Convention 28 June 2021

Quarles is talking specifically here about “stablecoins” but the observations might equally apply to the narrow bank or synthetic CBDC options that the BIS appears to find lacking. It is also important to note the qualification about ensuring that concerns with these kinds of digital currency are addressed. Quarles speech makes clear however that the in-principle argument for CBDC is far from clear to him:

To conclude, I emphasize three points. First, the U.S. dollar payment system is very good, and it is getting better. Second, the potential benefits of a Federal Reserve CBDC are unclear. Third, developing a CBDC could, I believe, pose considerable risks.

So, our work is cut out for us as we proceed to rigorously evaluate the case for developing a Federal Reserve CBDC. Even if other central banks issue successful CBDCs, we cannot assume that the Federal Reserve should issue a CBDC. The process that Chair Powell recently announced is a genuinely open process without a foregone conclusion, although obviously I think the bar to establishing a U.S. CBDC is a high one.

Quarles – “Parachute Pants and Central Bank Money”

The BIS in contrast appears to believe the case for CBDC has largely been made and the challenge is to figure out the best way to implement.

Money in the digital era

This section of the paper identifies “public interest”, defined broadly to include not only strict economic benefits flowing from competition and innovation but also political considerations like the right to privacy, as the overriding criterion by which change in the monetary system should be evaluated …

The overriding criterion when evaluating a change to something as central as the monetary system should be whether it serves the public interest. Here, the public interest should be taken broadly to encompass not only the economic benefits flowing from a competitive market structure, but also the quality of governance arrangements and basic rights, such as the right to data privacy.

… and then evaluates three innovations in digital money against that criterion. Firstly the growth in Bitcoin and other cryptocurrencies, secondly stablecoins and thirdly the entry of large technology firms (big techs) into payment services and financial services more generally.

The first two are quickly dismissed …

By now, it is clear that cryptocurrencies are speculative assets rather than money, and in many cases are used to facilitate money laundering, ransomware attacks and other financial crimes. Bitcoin in particular has few redeeming public interest attributes when also considering its wasteful energy footprint.

Stablecoins attempt to import credibility by being backed by real currencies. As such, these are only as good as the governance behind the promise of the backing. They also have the potential to fragment the liquidity of the monetary system and detract from the role of money as a coordination device. In any case, to the extent that the purported backing involves conventional money, stablecoins are ultimately only an appendage to the conventional monetary system and not a game changer.

The BIS assessment of cryptocurrencies is not a surprise but I wonder if the case for and against stablecoins might have deserved more detailed consideration. It is hard to argue with the observation that stablecoins are only as good as the governance behind the promise of their backing. This is however (as Quarles observes) something that could be addressed by regulation and supervision analogous to the way in which regulation and supervision underpins the integrity of the existing forms of digital currency created by private banks.

The potential for stablecoins to “fragment the liquidity of the monetary system” looks to be a more fundamental challenge and it would have been helpful to see a broader discussion of this concern. In the interests of full disclosure, I am talking my book here because this is an issue I raised previously but have not seen get much attention. I am guessing here, but the BIS conclusion that stablecoins backs by “conventional money” are at best “an appendage to the conventional monetary system” seems to be based on the premise that anything less than a direct liability of the central bank is just not worth trying. That might be right but a fuller explanation of the BIS perspective would have been useful.

The entry of big tech is, the BIS argues, the most significant development in large part due to the network effects and data insights that are part and parcel of the big tech business model.

…. the network effects that underpin big techs can be a mixed blessing for users. On the one hand, the DNA loop can create a virtuous circle, driving greater financial inclusion, better services and lower costs. On the other, it impels the market for payments towards further concentration.

The BIS nominates the high cost of digital payments as one area of concern

Entrenchment of market power may potentially exacerbate the high costs of payment services, still one of the most stubborn shortcomings of the existing payment system. An example is the high merchant fees associated with credit and debit card payments. Despite decades of ever-accelerating technological progress, which has drastically reduced the price of communication equipment and bandwidth, the cost of conventional digital payment options such as credit and debit cards remains high, and still exceeds that of cash

… basic access to digital payment services is another, especially for lower-income and other economically vulnerable groups

Related to the persistently high cost of some digital payment options is the lack of universal access to digital payment services. Access to bank and non-bank transaction accounts has improved dramatically over the past several decades, in particular in emerging market and developing economies (EMDEs). Yet in many countries, a large share of adults still have no access to digital payment options. Even in advanced economies, some users lack payment cards and smartphones to make digital payments, participate in e-commerce and receive transfers (such as government-to-person payments). For instance, in the United States, over 5% of households were unbanked in 2019, and 14% of adults did not use a payment card in 2017. In France, in 2017, 13% of adults did not own a mobile phone. Lower-income individuals, the homeless, migrants and other vulnerable groups are most likely to rely on cash. Due in part to market power and low expected margins, private PSPs often do not cater sufficiently to these groups. Remedies may necessitate public policy support as digital payments become more dominant.

… plus data governance and privacy concerns

The availability of massive amounts of user data gives rise to another important issue – that of data governance. Access to data confers competitive advantages that may entrench market power. Beyond the economic consequences, ensuring privacy against unjustified intrusion by both commercial and government actors has the attributes of a basic right. For these reasons, the issue of data governance has emerged as a key public policy concern.

Digital money is a central bank public good

This section of the paper lays out the BIS perspective on the role of the central bank in the monetary system. The foundation of the monetary system is trust in the currency which for the BIS is synonymous with trust in the central bank.

The foundation of the monetary system is trust in the currency. As the central bank provides the ultimate unit of account, that trust is grounded on confidence in the central bank itself. Like the legal system and other foundational state functions, the trust engendered by the central bank has the attributes of a public good. Such “central bank public goods” underpin the monetary system.

In its most tangible form, these central bank public goods take the form of the bank reserves that supply the ultimate means of payment for banks and the physical currency that circulates in the economy. Central banks also perform a variety of roles (operators, overseers and catalysts) by which they pursue key public interest objectives in the payments sphere: safety, integrity, efficiency and access.

The BIS identifies four key roles the central bank plays in pursuit of these objectives.

The first is to provide the unit of account in the monetary system. From that basic promise, all other promises in the economy follow.

Second, central banks provide the means for ensuring the finality of wholesale payments by using their own balance sheets as the ultimate means of settlement, as also reflected in legal concepts of finality (see glossary). The central bank is the trusted intermediary that debits the account of the payer and credits the account of the payee. Once the accounts are debited and credited in this way, the payment is final and irrevocable.

The third function is to ensure that the payment system works smoothly. To this end, the central bank provides sufficient settlement liquidity so that no logjams will impede the workings of the payment system, where a payment is delayed because the sender is waiting for incoming funds. At times of stress, the central bank’s role in liquidity provision takes on a more urgent form as the lender of last resort.

The central bank’s fourth role is to oversee the payment system’s integrity, while upholding a competitive level playing field. As overseer, the central bank imposes requirements on the participants so that they support the functioning of the payment system as a whole. Many central banks also have a role in the supervision and regulation of commercial banks, which are the core participants of the payment system. Prudential regulation and supervision reinforce the system. Further, in performing this role, central bank money is “neutral”, ie provided on an equal basis to all commercial parties with a commitment to competitive fairness.

The paper offers a brief overview of how a wholesale CBDC might operate. Wholesale CBDC are intended for the settlement of interbank transfers and related wholesale transactions and serve the same purpose as reserves held at the central bank but with added functionality such as conditional payment instructions. The focus of the paper is however on retail CBDCs…

Compared with wholesale CBDCs, a more far-reaching innovation is the introduction of retail CBDCs. Retail CBDCs modify the conventional two-tier monetary system in that they make central bank digital money available to the general public, just as cash is available to the general public as a direct claim on the central bank.

At least one part of the retail CBDC argument is pretty clear, they would offer users the lowest risk form of digital money (well lowest credit risk, inflation remains a risk with any form of fiat money).

A retail CBDC is akin to a digital form of cash, the provision of which is a core responsibility of central banks. Other forms of digital retail money represent a claim on an intermediary. Such intermediaries could experience illiquidity due to temporary lack of funds or even insolvency, which could also lead to payment outages. While such risks are already substantially reduced through collateralisation and other safeguards in most cases, retail CBDCs would put an end to any residual risk.

Retail CBDC come in two forms – “token” and “account” based

Retail CBDCs come in two variants … One option makes for a cash-like design, allowing for so-called token-based access and anonymity in payments. This option would give individual users access to the CBDC based on a password-like digital signature using private-public key cryptography, without requiring personal identification. The other approach is built on verifying users’ identity (“account-based access”) and would be rooted in a digital identity scheme. This second approach is more compatible with the monitoring of illicit activity in a payment system, and would not rule out preserving privacy: personal transaction data could be shielded from commercial parties and even from public authorities by appropriately designing the payment authentication process. These issues are intimately tied to broader policy debates on data governance and privacy, which we return to in a later section.

The BIS argues that the experience with operating Past Payment Systems (FPS) offers a guide for how to think about the introduction of a retail CBDC would affect crucial public interest issues like data governance, the competitive landscape of the PSPs and the industrial organisation of the broader payments industry. One of the lessons learned from the operation of FPS is that central banks should seek to facilitate the entry of new players.

… the experience of jurisdictions with a long history of operating retail FPS provides some useful lessons. Central banks can enhance the functioning of the monetary system by facilitating the entry of new players to foster private sector innovation in payment services. These goals could be achieved by creating open payment platforms that promote competition and innovation, ensuring that the network effects are channelled towards a virtuous circle of greater competition and better services.

The BIS argues that rules and standards that promote good data governance are among the key elements in establishing and maintaining open markets and a competitive level playing field. These include technical standards such as application programming interfaces (APIs) that impose a common format for data exchange from service providers. Together with data governance frameworks that assign ownership of data to users , these standards ensure interoperability of the services between Payment Service Providers.

Box III.B APIs and the industrial organisation of payments

An application programming interface … acts as a digital communication interface between service providers and their users. In its simplest form, a modern payment API first takes a request from an authorised user (eg a user who wants to send a friend money through a mobile banking app). It then sends the request to a server to obtain information (eg the friend’s bank account details or the sender’s account balance). Finally, it reports the retrieved information back to the user (the money has been sent).

APIs ensure the secure exchange of data and instructions between parties in digital interactions. Through encryption, they allow only the parties directly involved in a transaction to access the information transmitted. They accomplish this by ensuring proper authentication (verifying the credentials of the parties involved, eg from a digital ID, as discussed further in a later section) and authorisation (which specifies the resources a user is authorised to access or modify). Crucially, APIs can be set up to transmit only data relevant to a specific transaction. For example, a bank may provide an API that allows other banks to request the full name of the holder of a specific account, based on the account number provided. But this API will not allow the querying bank to retrieve the account holder’s home address or transaction history. Insofar as APIs provide strong security features, they can add an additional layer of security to interactions.

A key benefit of APIs is that they enable interoperability between different providers and simplify transactions. For example, many large financial institutions or big techs possess valuable consumer data, eg on payment transactions. By allowing other market participants to access and analyse data in order to develop and improve their products, APIs ensure a level playing field. This promotes competition and delivers benefits to consumers. An example is “open banking”, which allows third-party financial service providers to access transaction and other financial data from traditional financial institutions through APIs. For example, a fintech could use banks’ transaction data to assess credit risk and offer a loan at lower, more transparent rates than those offered by traditional financial institutions.

Payment APIs may offer software that allows organisations to create interoperable digital payment services to connect customers, merchants, banks and other financial providers

The BIS notes that the extent to which both CBDC and FPS can contribute to the public depends on an open payment system and the interoperability of the services offered by PSPs.

Well designed CBDCs and FPS have a number of features in common…

They both enable competing providers to offer new services through a range of interfaces – including in principle via prepaid cards and other dedicated access devices, as well as services that run on feature phones. Such arrangements not only allow for lower costs to users, but also afford universal access, and could thus promote financial inclusion.

Moreover, as the issuers of CBDCs and operators or overseers of FPS, central banks can lay the groundwork for assuring privacy and the responsible use of data in payments. The key is to ensure that governance for digital identity is appropriately designed. For both CBDC and FPS, such designs can incorporate features that support the smooth functioning of payment services without yielding control over data to private PSPs, as discussed above in the context of APIs. An open system that gives users control over their data can harness the DNA loop, breaking down the silos and associated market power of incumbent private firms with exclusive control over user data.

The BIS is at pains however to make the point (again) that central bank digital money is unique in a way that FPS et al cannot replicate …

Although CBDCs and FPS have many characteristics in common, one difference is that CBDCs extend the unique features and benefits of today’s digital central bank money directly to the general public. In a CBDC, a payment only involves transferring a direct claim on the central bank from one end user to another. Funds do not pass over the balance sheet of an intermediary, and transactions are settled directly in central bank money, on the central bank’s balance sheet and in real time. By contrast, in an FPS the retail payee receives final funds immediately, but the underlying wholesale settlement between PSPs may be deferred. This delay implies a short-term loan between parties, together with underlying credit risk on those exposures … : the payee’s bank credits its account in real time, while it has an account payable vis-à-vis the payer’s bank. In an FPS with deferred settlement, credit exposures between banks accumulate during the delay, for example over weekends. This exposure may be fully or partially collateralised – an institutional safeguard designed by the central bank.

The BIS acknowledges however that jurisdictions may weight the considerations discussed above differently …

Ultimately, whether a jurisdiction chooses to introduce CBDCs, FPS or other systems will depend on the efficiency of their legacy payment systems, economic development, legal frameworks and user preferences, as well as their aims. Based on the results of a recent survey, payments safety and financial stability considerations (also in the light of cryptocurrencies and stablecoins) tend to weigh more heavily in advanced economies. In EMDEs, financial inclusion is a more important consideration. Irrespective of the aims, an important point is that the underlying economics concerning the competitive landscape and data governance turn out to be the pivotal factors. These are shaped by the central bank itself.

CBDC architectures and the financial system

Designing a Retail CBDC requires that choices be made regarding who does what – the broad outline is that the central bank does the infrastructure while the private sector takes the customer facing role

Vital to the success of a retail CBDC is an appropriate division of labour between the central bank and the private sector. CBDCs potentially strike a new balance between central bank and private money. They will be part of an ecosystem with a range of private PSPs that enhances efficiency without impairing central banks’ monetary policy and financial stability missions. Central banks and PSPs could continue to work together in a complementary way, with each doing what they do best: the central bank providing the foundational infrastructure of the monetary system and the private PSPs using their creativity, infrastructure and ingenuity to serve customers.

A “two tier” system

… where the central bank and the private sector each play their respective role. A logical step in their design is to delegate the majority of operational tasks and consumer-facing activities to commercial banks and non-bank PSPs that provide retail services on a competitive level playing field. Meanwhile, the central bank can focus on operating the core of the system. It guarantees the stability of value, ensures the elasticity of the aggregate supply of money and oversees the system’s overall security.

Within this two tier framework, the BIS defines two models 1) A “Hybrid” and 2) an “Intermediated” CBDC architecture.

Under the Hybrid CBDC architecture

… the private sector onboards all clients, is responsible for enforcing AML/CFT regulations and ongoing due diligence, and conducts all retail payments in real time. However, the central bank also records retail balances. This “hybrid” CBDC architecture (Graph III.7, centre panel) allows the central bank to act as a backstop to the payment system. Should a PSP fail, the central bank has the necessary information – the balances of the PSP’s clients – allowing it to substitute for the PSP and guarantee a working payment system. The e-CNY, the CBDC issued by the People’s Bank of China and currently in a trial phase, exemplifies such a hybrid design

Under the Intermediated CBDC model …

… the central bank does not record retail transactions, but only the wholesale balances of individual PSPs (Graph III.7, bottom panel). The detailed records of retail transactions are maintained by the PSP. The benefits of such an “intermediated” CBDC architecture would be a diminished need for centralised data collection and perhaps better data security due to the decentralised nature of record-keeping – aspects that have been discussed in several advanced economies. By reducing the concentration of data, such designs could also enhance privacy (see next section). The downside is that additional safeguards and prudential standards would be necessary, as PSPs would need to be supervised to ensure at all times that the wholesale holdings they communicate to the central bank accurately reflect the retail holdings of their clients.

The PSPs in the Intermediated CBDC model operate customer wallets as a custodian rather than holding customer funds directly in the form of deposit liabilities. APIs ensure interoperability and data access between PSPs thereby avoiding closed networks. The BIS argues that the economic consequences of this model would be similar to those generated by existing retail FPS.

Centralised transaction ledger versus decentralised is another important design question; i.e. whether the transaction ledger recording who has paid what to whom and when is maintained by a trusted central authority or based on a decentralised governance system

Assessing the merits of each approach is an area of ongoing research. These studies also cover novel forms of decentralisation enabled via distributed ledger technology (DLT, see glossary). So-called permissioned DLT is envisioned in many current CBDC prototypes. In the process of updating the ledger of payment records, such permissioned DLT systems borrow concepts from decentralised cryptocurrencies, but remedy the problems due to illicit activity by allowing validation only by a network of vetted or permissioned validators.

Permissioned DLT designs may have economic potential in financial markets and payments due to enhanced robustness and the potentially lower cost of achieving good governance, as compared with systems with a central intermediary. However, such resilience does not come for free, as an effective decentralised design that ensures the right incentives of the different validators is costly to maintain. On balance, a trusted centralised design may often be superior, as it depends less on aligning the incentives of multiple private parties

Data governance will be issue whatever model model is chosen

The risks of data breaches would put an additional onus on the institutional and legal safeguards for data protection. This consideration also applies to today’s conventional payment system, in which PSPs store customer data. Yet data privacy and cyber resilience take on added importance in a system with a CBDC, especially on the part of the issuing central bank.

The BIS argues that these concerns can be addressed by incorporating varying degrees of anonymity into the CBDC design (as discussed in the next section).

The CBDC design must, the BIS argues, also address the consequences of dis-intermediating private banks

… the broader impact on financial intermediation activity is an important consideration in assessing the economic impact of CBDCs. Just like cash, CBDCs can be designed to maximise usefulness in payments, without giving rise to large inflows onto the central bank’s balance sheet. The design of CBDCs should further mitigate the systemic implications for financial intermediation, by ensuring that commercial banks can continue to serve as intermediaries between savers and borrowers. While cash offers safety and convenience in payments, it is not widely used as store of value. Today, consumers’ holdings of cash for payment purposes are in fact minimal in comparison with sight deposits at commercial banks…

The paper discusses a range of options for addressing this concern.

The BIS also notes that a design which “limits a CBDC’s footprint” would ensure that its issuance does not impair the monetary policy transmission process …

Instead, interest-bearing CBDCs would give central banks an additional instrument for steering real activity and inflation. If changes to the policy rate were directly passed through to CBDC remuneration, monetary transmission could be strengthened. There has also been discussion about the use of CBDCs to stimulate aggregate demand through direct transfers to the public. Rather than the use of the CBDC per se, the key challenge for such transfers is to identify recipients and their accounts. In any case, as CBDCs would coexist with cash, users would have access to either instrument, and it is unlikely that deeply negative interest rates would prevail, or that CBDC would materially change the effective lower bound on monetary policy rates.

At this stage, the BIS is pretty clear that the Two Tier model is the best choice …

Overall, a two-tiered architecture emerges as the most promising direction for the design of the overall payment system, in which central banks provide the foundations while leaving consumer-facing tasks to the private sector. In such a system, PSPs can continue to generate revenue from fees as well as benefiting from an expanded customer base through the provision of CBDC wallets and additional embedded digital services. A CBDC grounded in such a two-tiered system also ensures that commercial banks can maintain their vital function of intermediating funds in the economy.

… but undecided on Hybrid versus Intermediated models...

Both hybrid and intermediated models give central banks design options for sound data governance and high privacy standards. In either system, CBDCs could be supported by policy tools so that any unintended ramifications for the financial system and monetary policy could be mitigated.

Identification and privacy in CBDC design

The BIS’s approach to CBDC design starts with the principal that effective identification is crucial to ensure the systems safety and integrity and support efforts to counter money laundering and other illicit activities. This calls for a CBDC that is account based and tied to a digital identity while incorporating safeguards that protect data privacy.

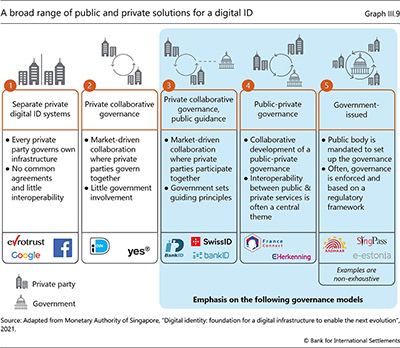

A digital ID might be constructed and verified in a variety of ways spanning the spectrum from systems that rely exclusively on private identities (e.g. big techs such as Google, Facebook, Alibaba, Tencent), to private-public partnerships, to government issued.

So identification (based on a unique digital ID) is crucial to the integrity of the payment system but there is a countervailing imperative to protect the privacy and safety of the users.

Beyond theft, the combination of transaction, geolocation, social media and search data raises concerns about data abuse and even personal safety. As such, protecting an individual’s privacy from both commercial providers and governments has the attributes of a basic right. In this light, preventing the erosion of privacy warrants a cautious approach to digital identity.

The BIS concludes that CBDC designs can protect the legitimate privacy of users by separating payment services from control over the resulting data.

Like some FPS, CBDCs could give users control over their payments data, which they need only share with PSPs or third parties as they decide (eg to support a credit application or other services). This can protect against data hoarding and abuse of personal data by commercial parties. Such designs can also prevent access by the central bank and other public authorities, while still allowing access by law enforcement authorities in exceptional cases – similar to today’s bank secrecy laws. In addition to the issue of who can access data, governance issues need to be addressed with respect to who holds the data. Concentration of data in the hands of a single entity puts an additional premium on the institutional and legal safeguards for data protection.

If desired, there are additional design features that could be adopted to further layers of anonymity even where the CBDC is account based.

One proposal is to ensure the anonymity of small-value transactions by issuing vouchers which are maintained by a separate data registrar that issues them up to some limit in the user’s name. Another approach, considered in the case of China’s e-CNY, is to shield the identity of the user by designating the user’s public key, which is issued by the mobile phone operator, as the digital ID. The central bank would not have access to the underlying personal details.

Summing up, the BIS concludes that the most promising design path is an account based CBDC built on a digital ID that is generated with official sector involvement. Different societies will however make different choices reflecting their different needs and preferences.

Digital ID could prove more efficient than physical documents, opening up many ways of supporting digital services in general. One size would not fit all in the choice of digital identification systems, as different societies will have different needs and preferences. A recent referendum in Switzerland illustrates this. While voters did not object to a digital ID in general, they rejected the proposal for one provided by the private sector.36 The foundational, public good nature of digital ID suggests that the public sector has an important role to play in providing or regulating such systems.

The international dimension of CBDC issuance

The report starts with the premise (generally accepted I think) that international payment services ….

“… do not work seamlessly across borders, as there are at times slow, expensive, opaque and cumbersome to use”

… so there is a clear opportunity for innovations that address these issues and that CBDCs could be part of the solution. That said, the BIS recognise that there are concerns that must be addressed if the CBDC solution is to serve the broader public interest.

Currency substition is a particular concern …

One potential concern is that the use of CBDCs across borders might exacerbate the risk of currency substitution, whereby a foreign digital currency displaces the domestic currency to the detriment of financial stability and monetary sovereignty. Indeed, a number of central banks see currency substitution – along with tax avoidance and more volatile exchange rates – as a key risk that they are addressing in their work on CBDCs

But the BIS believe that the currency substitution risk is manageable because a CBDC based on digital ID and implemented as an account based system would allow central banks to control the process of substitution in ways that they cannot do in the face of cash based subsititution risks they currently face. A foreign CBDC cannot circulate widely unless the central bank allows it to.

The cross-border use of account based CBDCs will however require international cooperation especially with regard to the use of digital ID information outside the originating country. The BIS recognises that a supranational digital ID is unlikely to be politically viable but argues that a cooperative approach based on mutual recognition of national ID credentials can work.

Such cooperation could form the basis for robust payment arrangements that tackle today’s challenges head-on. Of particular promise are multi-CBDC (mCBDC) arrangements that join up CBDCs to interoperate across borders. These arrangements focus on coordinating national CBDC designs with consistent access frameworks and interlinkages to make cross-currency and cross-border payments more efficient. In this way, they represent an alternative to private sector global stablecoin projects.

mCBDC arrangements would allow central banks to mitigate many of today’s frictions by starting from a “clean slate”, unburdened by legacy arrangements. There are three potential models. First, they could enhance compatibility for CBDCs via similar regulatory frameworks, market practices and messaging formats (Graph III.12, top panel). Second, they could interlink CBDC systems (middle panel), for example via technical interfaces that process end user-to-end user transactions across currency areas without going through any middlemen.

The greatest potential for improvement is offered by the third model, a single mCBDC system that features a jointly operated payment system hosting multiple CBDCs (bottom panel). FX settlements would be payment-versus-payment (PvP) by default, rather than requiring routeing or settlement instructions through a specific entity acting as an interface. Facilitating access and compatibility through such a system could benefit users through improved efficiency, lower costs and wider use of cross-border payments.

BIS data (April 2021) indicates that 11 out of 47 retail CBDC projects feature a cross-border dimension. Among the central banks pursuing this design feature, all three mCBDC arrangements are being considered but Model 2 seems to be the preferred choice possibly reflecting the reduced need for cooperation.

Conclusion

The BIS report concludes

Central banks stand at the centre of a rapid transformation of the financial sector and the payment system. Innovations such as cryptocurrencies, stablecoins and the walled garden ecosystems of big techs all tend to work against the public good element that underpins the payment system. The DNA loop, which should encourage a virtuous circle of greater access, lower costs and better services, is also capable of fomenting a vicious circle of entrenched market power and data concentration. The eventual outcome will depend not only on technology but on the underlying market structure and data governance framework.

Central banks around the world are working to safeguard public trust in money and payments during this period of upheaval. To shape the payment system of the future, they are fully engaged in the development of retail and wholesale CBDCs, alongside other innovations to enhance conventional payment systems. The aim of all these efforts is to foster innovation that serves the public interest.

CBDCs represent a unique opportunity to design a technologically advanced representation of central bank money, one that offers the unique features of finality, liquidity and integrity. Such currencies could form the backbone of a highly efficient new digital payment system by enabling broad access and providing strong data governance and privacy standards based on digital ID. To realise the full potential of CBDCs for more efficient cross-border payments, international collaboration will be paramount. Cooperation on CBDC designs will also open up new ways for central banks to counter foreign currency substitution and strengthen monetary sovereignty.