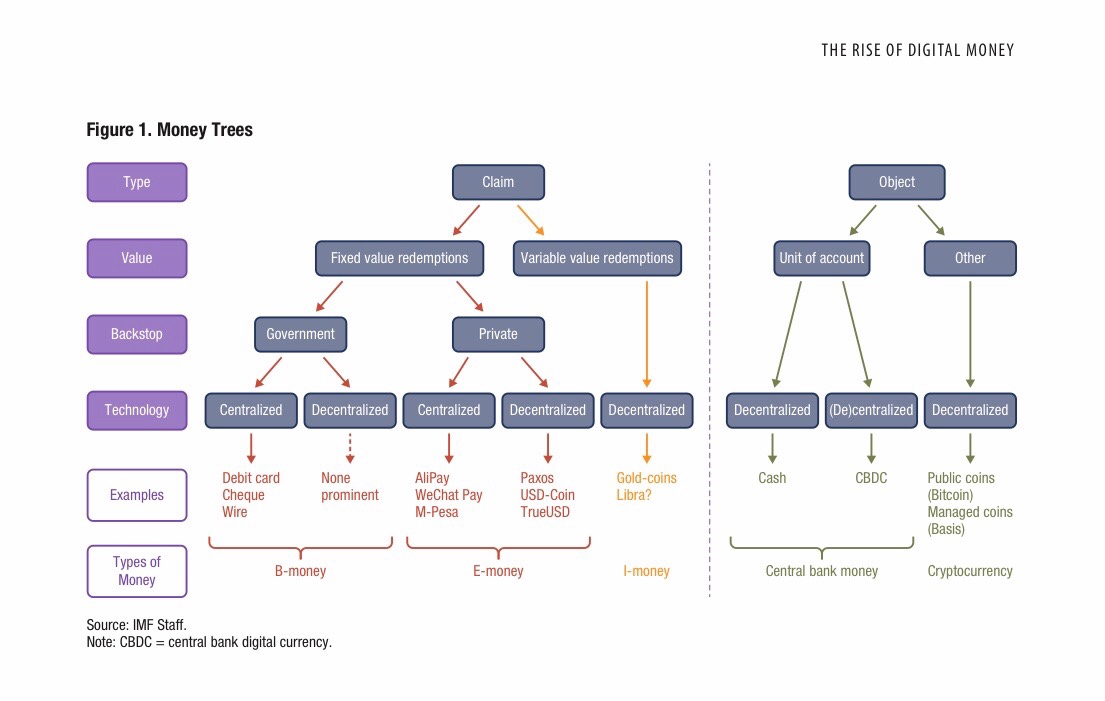

Well to be precise, the future of “payment stablecoins” seems to lie in some form of bank like regulation. That is one of the main conclusions to be drawn from reading the “Report on Stablecoins” published by the President’s Working Group on Financial Markets (PWG).

One of the keys to reading this report is to recognise that its recommendation are focussed solely on “payment stablecoins” which it defines as “… those stablecoins that are designed to maintain a stable value relative to a fiat currency and, therefore, have the potential to be used as a widespread means of payment.”

Some of the critiques I have seen from the crypto community argue that the report’s recommendations fail to appreciate the way in which stablecoin arrangements are designed to be self policing and cite the fact that the arrangements have to date withstood significant episodes of volatility without holders losing faith. Market discipline, they argue, makes regulation redundant and an impediment to experimentation and innovation.

The regulation kills innovation argument is a good one but what I think it misses is that the evidence in support of a market discipline solution is drawn from the existing uses and users of stablecoins which are for the most part confined to engaged and relatively knowledgeable participants. This group of financial pioneers have made a conscious decision to step outside the boundaries of the regulated financial system (with the protections that it offers) and can take the outcomes (positive and negative) without having systemic prudential impacts.

The PWG Report looks past the existing applications to a world in which stablecoins represent a material alternative to the existing bank based payment system. In this future state of the world, world stablecoins are being used by ordinary people and the question then becomes why this type of money is any different to private bank created money once it becomes widely accepted and the financial system starts to depend on it to facilitate economic activity.

The guiding principle is (not surprisingly) that similar types of economic activity should be subject to equivalent forms of regulation. Regulatory arbitrage rarely (if ever) ends up well. This is a sound basis for approaching the stablecoin question but it is not obvious to me that bank regulation is the right answer. To understand why, I recommend you read this briefing note published by Davis Polk (a US law firm), in particular the section titled “A puzzling omission” which explores the question why the Report appears to prohibit stablecoin issuers from structuring themselves as 100% reserve banks (aka “narrow banks”).

4. A puzzling omission.

By recommending that Congress require all stablecoin issuers to be IDIs, the Report would effectively require all stablecoin issuers to engage in fractional reserve banking and effectively prohibit them from being structured as 100% reserve banks (i.e., narrow banks9) that limit their activities to the issuance of stablecoins fully backed by a 100% reserve of cash or cash equivalents.10

The reason is that IDIs are subject to minimum leverage capital ratios that were calibrated for banks that engage in fractional reserve banking and invest the vast portion of the funds they raise through deposit-taking in commercial loans or other illiquid assets that are riskier but generate higher returns than cash or cash equivalents. Minimum leverage ratios treat cash and cash equivalents as if they had the same risk and return profile as commercial loans, commercial paper and long-term corporate debt, even though they do not. Unless Congress recalibrated the minimum leverage capital ratios to reflect the lower risk and return profile of IDIs that limit their assets to cash and cash equivalents, the minimum leverage capital ratios would make the 100% reserve model for stablecoin issuance uneconomic and therefore effectively prohibited.11 It is puzzling why the PWG, FDIC and OCC would recommend a regulatory framework that would effectively require stablecoin issuers to invest in riskier assets and rely on FDIC insurance rather than permitting stablecoins backed by a 100% cash and cash equivalent reserve.

This omission is puzzling for another reason. There has long been a debate whether deposit insurance schemes or a regime that required demand deposits to be 100% backed by cash or cash equivalents would be more effective in preventing runs or contagion. Indeed, the Roosevelt Administration, Senator Carter Glass, a number of economists and most well-capitalized banks were initially opposed to the proposal to create a federal deposit insurance scheme in 1933.12 Among the arguments against deposit insurance are that the benefits of deposit insurance in the form of reduced run and contagion risk are outweighed by the adverse effects in the form of reduced market discipline resulting from the reduced incentive of depositors to monitor the financial health of their banks. This reduced monitoring gives weaker banks more room to engage in risky activities the costs of which are borne by the stronger and more responsible banks in the form of excessive deposit insurance premiums or by taxpayers in the form of government bailouts.

In a competing proposal that has come to be known as the Chicago Plan, a group of economists led by economists at the University of Chicago argued in favor of a legal regime that required all demand deposits to be 100% backed by a reserve of cash or cash equivalents.13 Proponents of the Chicago Plan argued that it would be more effective in stemming runs and contagion than the proposed federal deposit insurance scheme, without undermining market discipline or creating moral hazard. The Chicago Plan would have been analogous to the original National Bank Act that required all paper currency issued by national banks to be fully backed 100% by U.S. Treasury securities. The Chicago Plan was ultimately rejected in favor of the federal deposit insurance scheme that was enacted in 1933 not because it would have been less effective than deposit insurance in stemming runs and contagion, but because it was viewed as too radical. Policymakers feared that by prohibiting banks from using deposits to fund commercial loans and invest in other debt instruments, the Chicago Plan would have resulted in a further contraction in the already severely contracted supply of credit that was fueling the great contraction in economic output that later became known as the Great Depression.

It is understandable why the Report does not recommend prohibiting IDIs from issuing, transferring or buying and selling stablecoins that represent insured deposit liabilities. What is puzzling in light of this history, however, is why the Report would effectively prohibit stablecoin issuers from structuring themselves as 100% reserve (i.e., narrow) banks that limit their activities to the issuance, transfer and buying and selling stablecoins fully backed by a 100% reserve of cash or cash equivalents.

“U.S. regulators speak on stableman and crypto regulation” Davis Polk Client Update, 12 November 2021

I am open to the possibility that the conventional bank regulation solution was unintended and that a narrow bank option might still be on the table. In that regard, I note that Circle has been pursuing the 100% reserve bank option for some time already so it would have been reasonable to expect that the PWG Report to discuss why this was not an option if they were ruling it out. The value of the Davis Polk note is that it neatly explains why being required to operate under bank regulation (the Leverage Ratio in particular) will be problematic for the stablecoin business model. This will be especially useful for those in the stablecoin community who may believe that fractional reserve banking is a free option to increase the riskiness of the assets that back the stablecoin liabilities.

But, as always, I may be missing something…

Tony – From the Outside