The ability to raise funding via deposit accounts is one of the things that makes banks different from other types of companies. This post explores the mechanics of how an unsecured loan to a highly leveraged company (i.e. a bank deposit) can be transformed into an (arguably) risk free asset. The focus will be on AUD denominated deposits held with APRA authorised deposit-taking institutions incorporated in Australia (“Australian ADIs” or “Australian banks”).

I thought I understood the process pretty well but writing it down is a good way to see if it all makes sense. Documenting my understanding also creates a platform for others to tell me what I have missed or mis-understood.

The most user friendly source of insight I could find was an article by Grant Turner published in the RBA Bulletin (December 2011) titled “Depositor Protection in Australia” which summarised the position as follows …

“Depositors in authorised deposit-taking institutions (ADIs) in Australia benefit from a number of layers of protection … At the broadest level, Australia has a strong system of prudential regulation and supervision which, together with sound management at individual institutions, has meant that problems in ADIs have been rare. In addition, depositors benefit from strong protections in the unlikely event that an ADI fails. They have a priority claim on the assets of a failed ADI ahead of other unsecured creditors, known as ‘depositor preference’. Depositor protection arrangements were further strengthened in 2008 with the introduction of the Financial Claims Scheme (FCS), under which the Australian Government guarantees the timely repayment of deposits up to … $250,000 per person per ADI ….

Depositor Protection in Australia, Grant Turner, RBA Bulletin December Quarter 2011 (p45).

So AUD denominated bank deposits with Australian banks are engineered to be safe because

- the banks are subject to a strong system of prudential regulation,

- the deposits themselves have a priority super senior claim on the assets of the bank should it fail, and

- the timely repayments of AUD deposits up to $250,000 per person per bank is guaranteed by the Australian Government.

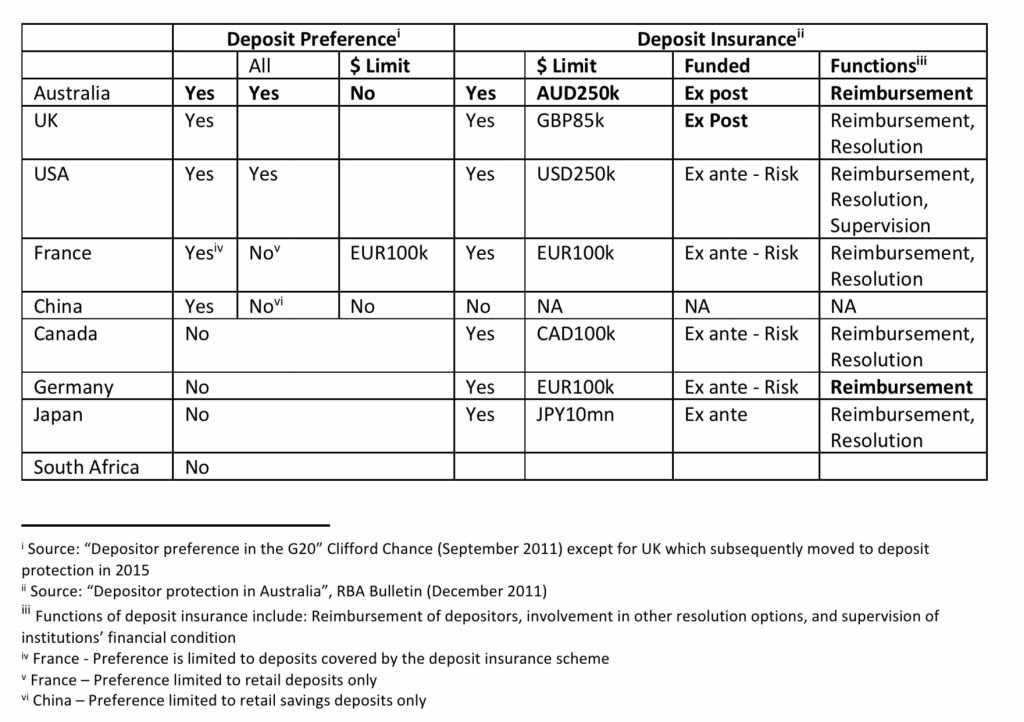

Deposit preference and deposit insurance – not all deposits are created equal

While it is common for deposits to have some degree of protection, the precise details vary across different jurisdictions and some, like New Zealand, for a long time eschewed any special treatment as a point of principle.

The table below is a work in progress but I found it useful to compare the Australian approach to deposit protection with that developed in a small selection of other jurisdictions.

The features to note:

- Some form of deposit guarantee is relatively common but deposit preference less so – Australia offers both deposit preference and insurance,

- Australia’s approach to deposit preference is at the more supportive end of the spectrum both because it applies to all types of deposits (some jurisdictions only protect retail depositors) and because it applies without any value limit (some jurisdictions only protect guaranteed deposit balances),

- Australia’s approach to deposit insurance is funded on ex post basis (ex ante seems to be more common) and the insurance is only applied to reimburse depositors for any shortfall relative to their preferred claim on the assets of the bank.

Deposits are government guaranteed – what more do I need to know?

I suspect that people who pay any attention to the topic are aware that Australian bank deposits are guaranteed by the government. For most people that is probably enough – a government guarantee is as safe as it gets (unless of course you want to go with gold or other precious metals).

When you look at the detail, the role the government guarantee plays in underwriting the safety of bank deposits seems pretty limited. The guarantee only comes into play if a series of conditions are met, including that APRA consider that the ADI is insolvent and that the Treasurer determines that it is necessary to deploy the guarantee.

In practice, recourse to the guarantee might be required for a small ADI heavily reliant on deposit funding but I suspect that this chain of events is extremely unlikely to play out for one of the bigger banks. That is partly because the risk of insolvency has been substantially reduced by higher CET1 requirements but also because APRA as the agent of the government now has a range of tools that allow it to bail-in rather than bail-out bank creditors that rank below depositors in the loss hierarchy.

If you want to understand why (or whether) deposits with the bigger ADIs are safe then I think the answers lie in:

- the Banking Act and

- changes to bank capital adequacy requirements implemented to address the bail-out problem that confronted the world during the GFC

The Banking Act 1959.

In order to understand the mechanics of why bank deposits can be low risk, independent of the government guarantee, we first head down the rabbit hole into the Banking Act 1959. This is not a journey for the faint of heart but understanding exactly what the Australian Banking Act says creates a foundation for understanding some of the economics of the funding instruments that rank below deposits.

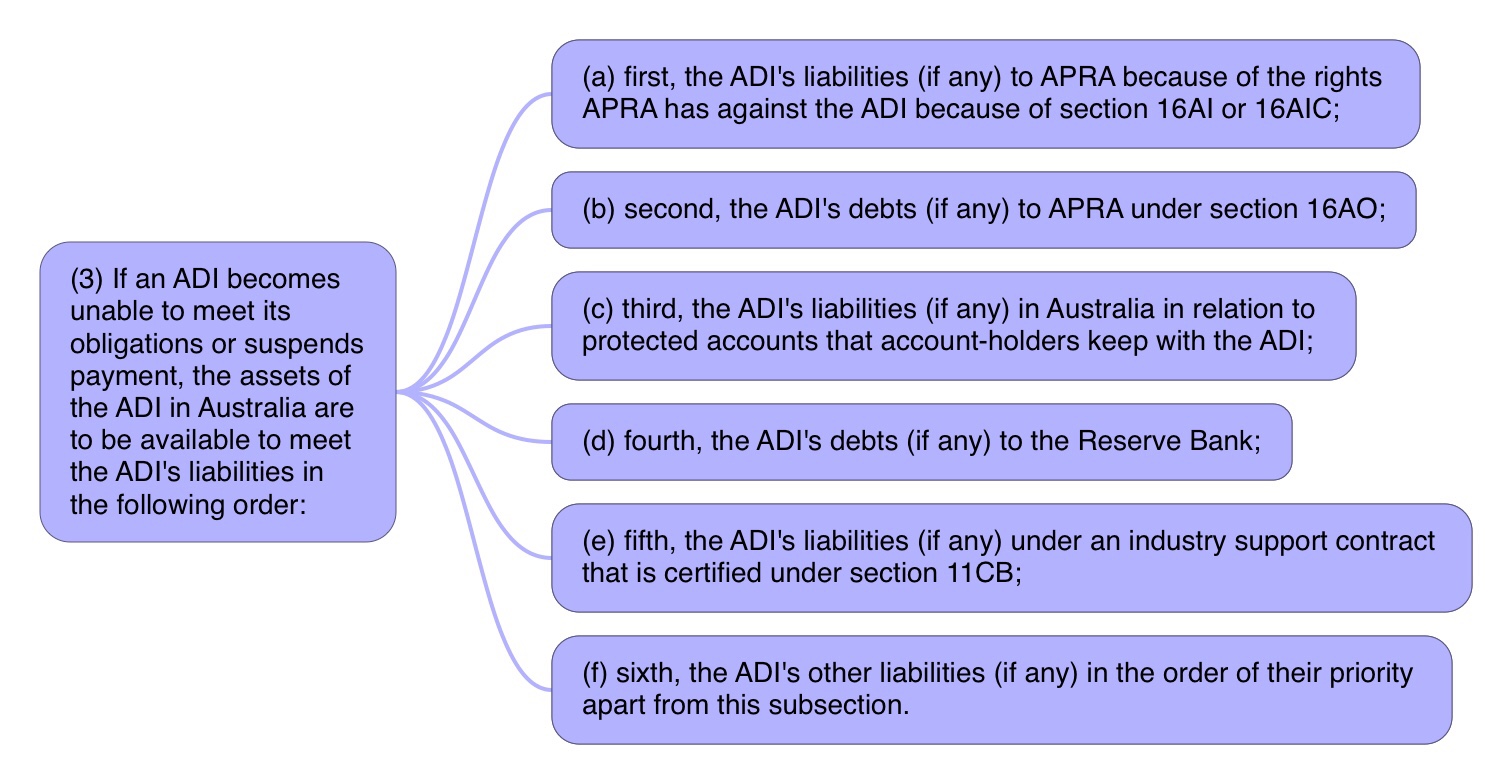

Section 13A which sets out the “Consequences of inability or failure of ADI etc. to meet certain requirements” and Subsection 3 in particular is a good place to start …

This part of the Banking Act defines the priority of the claims against an ADI should it fail to honour its obligations but it does not contain any explicit reference to deposits. There is however a reference (Subsection 3(c)) to “protected accounts” that account holders keep with the Australian part of the ADI.

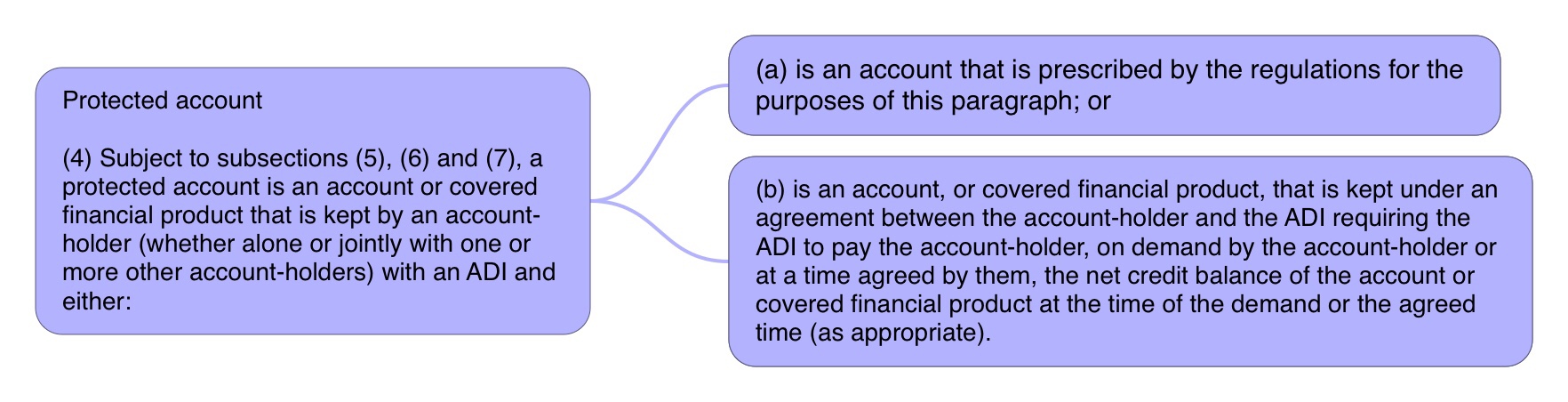

The definition of a “protected account” can be found in Section 5 (Interpretation) – Subsection 4.

Still no explicit reference to deposits but the focus on an “account” kept by an account holder with an ADI sounds like a deposit and builds on the idea of a “banker customer relationship” which I am reliably advised is an established concept under Australian law. I also tracked down a copy of a “Declaration of Covered Financial Products” dated 27 October 2008 which has a long list of accounts that we would recognise as bank deposits accounts.

Further support for concluding that a bank deposit is a “protected account” assigned a preference under Section 13A can be found in a proposed amendment to the Banking Act that includes the following definition:

“deposit account means an account that is kept

(a) by an account-holder (whether alone or jointly with one or more other account-holders) with an ADI; and

(b) under an agreement between the account-holder and the ADI, requiring the ADI to pay the account-holder, on demand by the account-holder or at a time agreed by them, the net credit balance of the account at the time of the demand or the agreed time (as appropriate).”

Banking Amendment (Deposits) Bill 2020 No. , 2020

Summing up, the Banking Act does not (as yet) explicitly say that deposits are protected but that is I think a robust conclusion once you work through the detail.

Prudential Regulation

Prudential capital adequacy can be complicated but I will focus on two concepts employed by APRA that, in combination with deposit preference, seem to me to be the key to the safety of bank deposits held with the big ADIs.

The first is the “Unquestionably Strong” benchmark for Common Equity Tier 1 (CET1) capital that was developed in response to one of the recommendations of the 2014 Financial System Inquiry. The increased capital that ADIs have built up in response to the Unquestionably Strong benchmark has made a substantial contribution to reducing the risk that an ADI might ever be unable to honour its commitments to repay its liabilities.

The second element is the development of a supplementary layer of loss absorbing capital that will only come into play in the event that an ADI has been identified as being “non-viable”. This is in many respects one of the more interesting (though possibly less well understood) components of the prudential tool kit because it directly addresses the problem of banks being too big to fail.

This TBTF problem is why I suspect that that the government guarantee will probably never by a practical option if one of the big ADIs get into trouble. Apart from the disruption to customers and the economy, liquidating a big bank will likely unnecessarily destroy huge amounts of value. Failure is rendered somewhat remote given the Unquestionably Strong benchmark for CET1 but, in the event that a big ADI did find some way to blow itself up, it seem much more likely APRA would choose to bail-in the investors who had signed up to underwriting the risk.

Summing up

Deposits held with Australian banks are at face value a risky asset given that they are an unsecured loan to a highly leverage company. In practice that risk is substantially reduced by virtue of the fact that:

- the banks are subject to a strong system of prudential regulation including the requirement to meet an “Unquestionably Strong” benchmark for CET1 capital supplemented by a substantial pool of additional loss absorbing capital that can be bailed-in if required,

- the deposits themselves have a priority super senior claim on the assets of the bank should it fail, and

- the timely repayments of AUD deposits up to $250,000 per person per bank is guaranteed by the Australian Government.

The government guarantee is probably the feature that most people take comfort from but I have argued that the super senior claim combined with the strong system of prudential capital adequacy regulation probably counts for more if you hold a deposit account at one of the bigger ADIs.

Editing Note: As always, the risk remains that I am missing something and I suspect that I will probably revise this post many times before I am entirely happy with it.

Appendices – Digging further into the detail

Appendix 1 – What about liabilities to APRA?

The only liabilities that rank ahead of bank deposits are certain liabilities to APRA including costs that APRA incurs in the exercise of the powers it employs pursuant to Section 13A of the act (see above). These liabilities are defined elsewhere in the Banking Act but, so far as I can determine, the most material of them is likely to be liabilities that APRA takes over from depositors of a failed ADI pursuant to the operation of the Government guarantee of deposits under the Financial Claims Scheme (FCS).

What happens in the FCS is that APRA takes over the responsibility for repayment of guaranteed deposit balances from the ADI and then takes the place of those depositors at the head of the queue for payment from the proceeds of liquidating the failed bank. Again I will refer to Grant Turner’s article for a concise description of the process …

“Payouts of deposits covered under the FCS are initially financed by the Government through a standing appropriation of $20 billion per failed ADI (although it is possible that additional funds could be made available, if needed, subject to parliamentary approval). The amount paid out under the FCS, and expenses incurred by APRA in connection with the FCS, would then be recovered via a priority claim of the Government against the assets of the ADI in the liquidation process. If the amount realised is insufficient, the Government can recover the shortfall through a levy on the ADI industry

Depositor Protection in Australia, Grant Turner, RBA Bulletin December Quarter 2011 (p53)

Technically speaking, the deposit balances in excess of the $250,000 government guarantee rank behind the guaranteed deposits but this does not change the fact that a lot of equity and other liabilities issued by the ADI have to be wiped out before the capacity to repay deposit principal in full is called into question.

Appendix 2 – What about covered bonds?

Covered bonds are typically seen as lower risk than bank deposits above the guarantee threshold by virtue of the fact that they are explicitly secured by a specified pool of high quality assets. Their security is achieved at the expense of bank deposits that would otherwise have had a preferred claim on the assets transferred into the covered bond pool. This is also why APRA was careful to place strict limits on how much covered bonds an ADI could issue.

The only qualification I would make on the general principle that covered bonds are less risky is that, while bank deposits are technically unsecured, they do still very much benefit from their deeply senior position in the bank loss hierarchy sitting as they do at the end of a chain of more junior components starting with common equity and running progressively through Additional Tier 1 capital, Tier 2 capital and senior debt. Bank deposits are technically unsecured but, depending on the specific funding structure of the issuing bank, they can be heavily over-collateralised.

The general proposition that bank deposits in excess of the government guarantee are still relatively low risk by virtue of their super senior claim and high level of over-collateralisation is based on what we observe for the major Australian banks. The extent to which this argument also applies to the smaller Australian banks depends on the precise details of their liability structure. As a rule, I would expect to see more reliance on deposit funding and hence less over-collateralisation but I need to do more work to test this hypothesis.

Appendix 3 – Why do we give bank deposits this privilege?

The first point to note is that not all banking systems incorporate the deposit preference principle. The usual argument against deposit protection is that it creates moral hazard.

A financial system that creates moral hazard is clearly undesirable but it is less clear to me that bank depositors are the right set of stakeholders to take on the responsibility of imposing market discipline on banks. There is a very real problem here but requiring depositors to take on this task is not the answer. It is also important I think to recognise that deposit preference moves the risk to other parts of the balance sheet that are arguably better suited to the task of exercising market discipline.

I have addressed this question in more detail in this post.