The Australian Government’s 2014 Financial System Inquiry (FSI) recommended that APRA implement a framework for minimum loss-absorbing and recapitalisation capacity in line with emerging international practice, sufficient to facilitate the orderly resolution of Australian authorised deposit-taking institutions (ADIs) and minimise taxpayer support (Recommendation 3).

In early November, APRA released a discussion paper titled “Increasing the loss absorption capacity of ADIs to support orderly resolution” setting out its response to this recommendation. The paper proposes that selected Australian banks be required to hold more loss absorbing capital. Domestic Systemically Important Banks (DSIBs) are the primary target but, depending partially on how their Recovery and Resolution Planning addresses the concerns APRA has flagged, some other banks will be captured as well.

The primary objectives are to improve financial safety and stability but APRA’s assessment is that competition would also be “Marginally improved” on the basis that “requiring larger ADIs to maintain additional loss absorbency may help mitigate potential funding advantages that flow to larger ADIs“. This assessment may be shaped by the relatively modest impact (5bp) on aggregate funding costs that APRA has estimated or simple regulatory conservatism. I suspect however that APRA is under selling the extent to which the TBTF advantage would be mitigated if not completely eliminated by the added layer of loss absorption proposed. If I am correct, then this proposal would in fact, not only minimise the risk to taxpayers of future banking crises, but also represent an important step forward in placing Australian ADIs on a more level playing field.

Why does the banking system need more loss absorption capacity?

APRA offers two reasons:

- The critical role financial institutions play in the economy means that they cannot be allowed to fail in a disorderly manner that would have adverse systemic consequences for the economy as a whole.

- The government should not be placed in a position where it believes it has no option but to bail out one or more banks

The need for extra capital might seem counter-intuitive, given that ADI’s are already “unquestionably strong”, but being unquestionably strong is not just about capital, the unstated assumption is that the balance sheet and business model are also sound. The examples that APRA has used to calibrate the degree of total loss absorption capacity could be argued to reflect scenarios in which failures of management and/or regulation have resulted in losses much higher than would be expected in a well-managed banking system dealing with the normal ups and downs of the business cycle.

At the risk of over simplifying, we might think of the first layers of the capital stack (primarily CET1 capital but also Additional Tier 1) being calibrated to the needs of a “good bank” (i.e. well-managed, well-regulated) while the more senior components (Tier 2 capital) represent a reserve to absorb the risk that the good bank turns out to be a “bad bank”.

What form will this extra capital take?

APRA concludes that ADI’s should be required to hold “private resources” to cope with this contingency. I doubt that conclusion would be contentious but the issue is the form this self-insurance should take. APRA proposes that the additional loss absorption requirement be implemented via an increase in the minimum Prudential Capital Requirement (PCR) applied to the Total Capital Ratio (TCR) that Authorised Deposit-Taking Institutions (ADIs) are required to maintain under Para 23 of APS 110.

“The minimum PCRs that an ADI must maintain at all times are:

(a) a Common Equity Tier 1 Capital ratio of 4.5 per cent;

(b) a Tier 1 Capital ratio of 6.0 per cent; and

(c) a Total Capital ratio of 8.0 per cent.

APRA may determine higher PCRs for an ADI and may change an ADI’s PCRs at any time.”

APS 110 Paragraph 23

This means that banks have discretion over what form of capital they use, but APRA expect that banks will use Tier 2 capital that counts towards the Total Capital Ratio as the lowest cost way to meet the requirement. Advocates of the capital structure irrelevance thesis would likely take issue with this part of the proposal. I believe APRA is making the right call (broadly speaking) in supporting more Tier 2 rather than more CET1 capital, but the pros and cons of this debate are a whole post in themselves. The views of both sides are also pretty entrenched so I doubt I will contribute much to that 50 year old debate in this post.

How much extra loss absorbing capital is required?

APRA looked at three things when calibrating the size of the additional capital requirement

- Losses experienced in past failures of systemically important banks

- What formal requirements other jurisdictions have applied to their banks

- The levels of total loss absorption observed being held in an international peer group (i.e. what banks choose to hold independent of prudential minimums)

Based on these inputs, APRA concluded that requiring DSIBs to maintain additional loss absorbing capital of between 4-5 percentage points of RWA would be an appropriate baseline setting to support orderly resolution outcomes. The calibration will be finalised following the conclusion of the consultation on the discussion paper but this baseline requirement looks sufficient to me based on what I learned from being involved in stress testing (for a large Australian bank).

Is more loss absorption a good idea?

The short answer, I think, is yes. The government needs a robust way to recapitalise banks which does not involve risk to the taxpayer and the only real alternative is to require banks to hold more common equity.

The devil, however, is in the detail. There are a number of practical hurdles to consider in making it operational and these really need to be figured out (to the best of out ability) before the fact rather than being made up on the fly under crisis conditions. The proposal also indirectly raises some conceptual issues with capital structure that are worth understanding.

How would it work in practice?

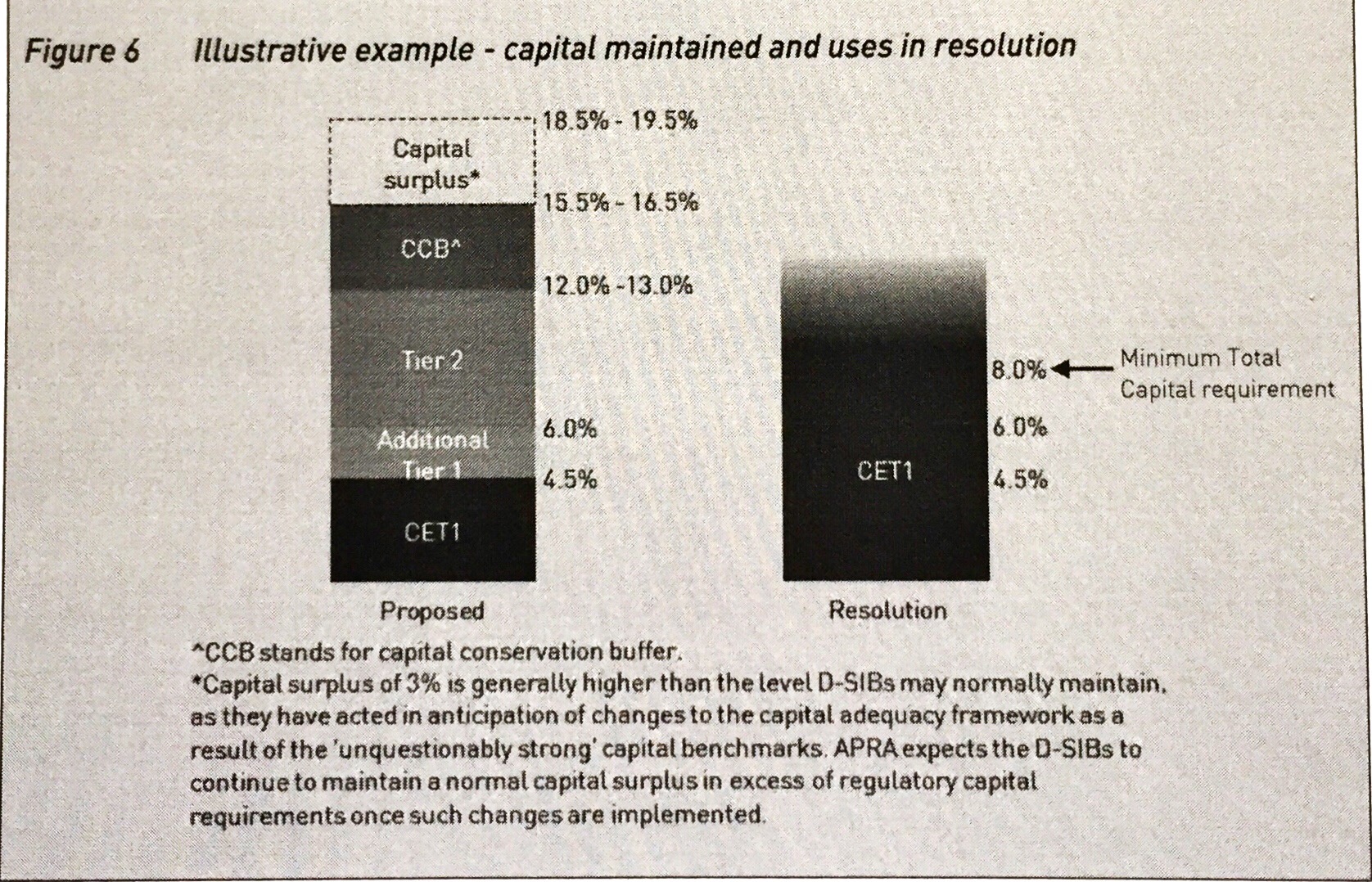

The discussion paper sets out “A hypothetical outcome from resolution action” to explain how an orderly resolution could play out.

“The approximate capital levels the D-SIBs would be expected to maintain following an increase to Total Capital requirements, and a potential outcome following the use of the additional loss absorbency in resolution, are presented in Figure 6. Ultimately, the outcome would depend on the extent of losses.

If the stress event involved losses consistent with the largest of the FSB study (see Figure 2), AT1 and Tier 2 capital instruments would be converted to ordinary shares or written off. After losses have been considered, the remaining capital position would be wholly comprised of CET1 capital. This conversion mechanism is designed to allow for the ADI to be stabilised in resolution and provide scope to continue to operate, and particularly to continue to provide critical functions.”

Source – APRA Discussion Paper (page 24)

What I have set out below draws from APRA’s example while adding detail that hopefully adds some clarity on what should be expected if these scenarios ever play out.

- In a stress event, losses first impact any surplus CET1 held in excess of the Capital Conservation Buffer (CCB) requirement, and then the CCB itself (the first two layers of loss absorption in Figure 6 above)

- As the CCB is used up, the ADI is subject to progressive constraints on discretionary distributions on CET1 and AT1 capital instruments

- In the normal course of events, the CCB should be sufficient to cope with most stresses and the buffer is progressively rebuilt through profit retention and through new issuance, if the ADI wants to accelerate the pace of the recapitalisation process

- The Unquestionably Strong capital established to date is designed to be sufficient to allow ADIs to withstand quite severe expected cyclical losses (as evidenced by the kinds of severe recession stress scenarios typically used to calibrate capital buffers)

- In more extreme scenarios, however, the CCB is overwhelmed by the scale of losses and APRA starts to think about whether the ADI has reached a Point of Non-Viability (PONV) where ADI’s find themselves unable to fund themselves or to raise new equity; this is where the proposals in the Discussion Paper come into play

- The discussion paper does not consider why such extreme events might occur but I have suggested above that one reason is that the scale of losses reflects endogenous weakness in the ADI (i.e. failures of risk management, financial control, business strategy) which compound the losses that would be a normal consequence of downturns in the business cycle

- APRA requires that AT1 capital instruments, classified as liabilities under Australian Accounting Standards, must include a provision for conversion into ordinary shares or write off when the CET1 capital ratio falls to, or below 5.125 per cent

- In addition, AT1 and Tier 2 capital instruments must contain a provision, triggered on the occurrence of a non-viability trigger event, to immediately convert to ordinary shares or be written off

- APRA’s simple example show both AT1 and Tier 2 being converted to CET1 (or write-off) such that the Post Resolution capital structure is composed entirely of CET1 capital

Note that conversion of the AT1 and Tier 2 instruments does not in itself allocate losses to these instruments. The holders receive common equity equivalent to the book value of their instrument which they can sell or hold. The ordinary shareholders effectively bear the loss via the forced dilution of their shareholdings. The main risk to the ATI and Tier 2 holders is that, when they sell the ordinary shares received on conversion, they may not get the same price that which was used to convert their instrument. APRA also imposes a floor on the share price that is used for conversion which may mean that the value of ordinary shares received is less than the face value of the instrument being converted. The reason why ordinary shareholders should be protected in this way under a resolution scenario is not clear.

The devil is in the detail – A short (probably incomplete) list of issues I see with the proposal:

- Market capacity to supply the required quantum of additional Tier 2 capital required

- Conversion versus write-off

- The impact of conversion on the “loss hierarchy”

- Why not just issue more common equity?

- To what extent would the public sector continue to stand behind the banking system once the proposed level of self insurance is in place?

Market capacity to supply the required level of additional loss absorption

APRA has requested industry feedback on whether market appetite for Tier 2 capital will be a problem but its preliminary assessment is that:

” … individual ADIs and the industry will have the capacity to implement the changes necessary to comply with the proposals without resulting in unnecessary cost for ADIs or the broader financial system.

Preliminary estimates suggest the total funding cost impact from increasing the D-SIBs’Total Capital requirements would not be greater than five basis points in aggregate based on current spreads. Assuming the D-SIBs meet the increased requirement by increasing the issuance of Tier 2 capital instruments and reducing the issuance of senior unsecured debt, the impact is estimated by observing the relative pricing of the different instruments. The spread difference between senior unsecured debt and Tier 2 capital instruments issued by D- SIBs is around 90 to 140 basis points.”

I have no expert insights on this question beyond a gut feel that the required level of Tier 2 capital cannot be raised without impacting the current spread between Tier 2 capital and senior debt, if at all. The best (only?) commentary I have seen to date is by Chris Joye writing in the AFR (see here and here). The key points I took from his opinion pieces are:

- The extra capital requirement translates to $60-$80 billion of extra bonds over the next four years (on top of rolling over existing maturities)

- There is no way the major banks can achieve this volume

- Issuing a new class of higher ranking (Tier 3) bonds is one option, though APRA also retains the option of scaling back the additional Tier 2 requirement and relying on its existing ability to bail-in senior debt

Chris Joye know a lot more about the debt markets than I do, but I don’t think relying on the ability to bail-in senior debt really works. The Discussion Paper refers to APRA’s intention that the “… proposed approach is … designed with the distinctive features of the Australian financial system in mind, recognising the role of the banking system in channelling foreign savings into the economy “ (Page 4). I may be reading too much into the tea leaves, but this could be interpreted as a reference to the desirability of designing a loss absorbing solution which does not adversely impact the senior debt rating that helps anchor the ability of the large banks to borrow foreign savings. My rationale is that the senior debt rating impacts, not only the cost of borrowing, but also the volume of money that foreign savers are willing to entrust with the Australian banking system and APRA specifically cites this factor as shaping their thinking. Although not explicitly stated, it seems to me that APRA is trying to engineer a solution in which the D-SIBs retain the capacity to raise senior funding with a “double A” rating.

Equally importantly, the creation of a new class of Tier 3 instruments seems like a very workable alternative to senior bail-in that would allow the increased loss absorption target to be achieved without impacting the senior debt rating. This will be a key issue to monitor when ADI’s lodge their response to the discussion paper. It also seems likely that the incremental cost of the proposal on overall ADI borrowing costs will be higher than the 5bp that APRA included in the discussion paper. That is not a problem in itself to the extent this reflects the true cost of self insurance against the risk of failure, just something to note when considering the proposal.

Conversion versus write-off

APRA has the power to effect increased loss absorption in two ways. One is to convert the more senior elements of the capital stack into common equity but APRA also has the power to write these instruments off. Writing off AT1 and/or T2 capital, effectively represents a transfer of value from the holders of these instruments to ordinary shareholders. That is hard to reconcile with the traditional loss hierarchy that sees common equity take all first losses, with each of the more senior tranches progressively stepping up as the capacity of more junior tranches is exhausted.

Consequently I assume that the default option would always favour conversion over write-off. The only place that I can find any guidance on this question is Attachment J to APS 111 (Capital Adequacy) which states

Para 11. “Where, following a trigger event, conversion of a capital instrument:

(a) is not capable of being undertaken;

(b) is not irrevocable; or

(c) will not result in an immediate and unequivocal increase in Common Equity Tier 1 Capital of the ADI,

the amount of the instrument must immediately and irrevocably be written off in the accounts of the ADI and result in an unequivocal addition to Common Equity Tier 1 Capital.”

That seems to offer AT1 and Tier 2 holders comfort that they won’t be asked to take losses ahead of common shareholders but the drafting of the prudential standard could be clearer if there are other reasons why APRA believe a write-off might be the better resolution strategy. The holders need to understand the risks they are underwriting but ambiguity and uncertainty are to helpful when the banking system is in, or a risk of, a crisis.

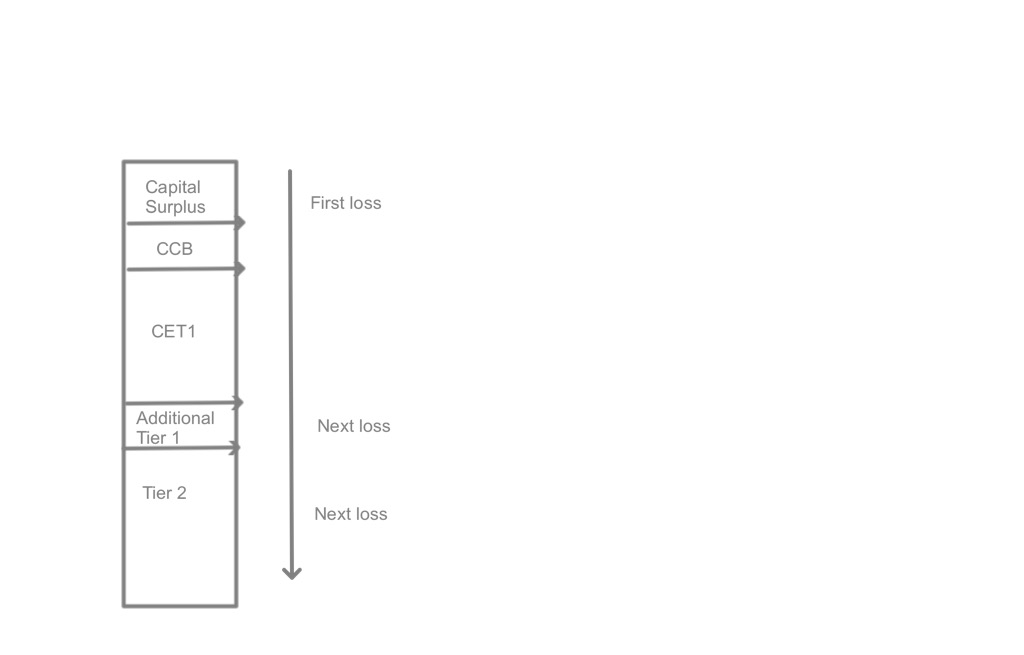

The impact of conversion on the “loss hierarchy”

The concept of a loss hierarchy describes the sequence under which losses are first absorbed by common equity and then by Additional Tier 1 and Tier 2 capital, if the more junior elements prove insufficient. Understanding the loss hierarchy is I think fundamental to understanding capital structure in general and this proposal in particular:

- In a traditional liquidation process, the more senior elements should only absorb loss when the junior components of the capital stack are exhausted

- In practice, post Basel III, the more senior elements will be required to participate in recapitalising the bank even though there is still some book equity and the ADI technically solvent (though not necessarily liquid)

- This is partly because the distributions on AT1 instruments are subject to progressively higher capital conservation restrictions as the CCB shrinks but mostly because of the potential for conversion to common equity (I will ignore the write-off option to keep things simple)

I recognise that APRA probably tried to simplify this explanation but the graphic example they used (see Figure 6 above) to explain the process shows the Capital Surplus and the CCB (both CET1 capital) sitting on top of the capital stack followed by Tier 2, Additional Tier 1 and finally the minimum CET1 capital. The figure below sets out what I think is a more logical illustration of the capital stack and loss .

Losses initially impact CET1 directly by reducing net tangible assets per share. At the point of a non-viability based conversion event, the losses impact ordinary shareholders via the dilution of their shareholding. AT1 and Tier 2 holders only share in these losses to the extent that they sell the ordinary shares they receive for less than the conversion price (or if the conversion price floor results in them receiving less than the book value of their holding).

Why not just issue more common equity?

Capital irrelevancy M&M purists will no doubt roll their eyes and say surely APRA knows that the overall cost of equity is not impacted by capital structure tricks. The theory being that any saving in the cost of using lower cost instruments, will be offset by increases in the costs (or required return) of more subordinated capital instruments (including equity).

So this school argues you should just hold more CET1 and the cost of the more senior instruments will decline. The practical problem I think is that, the cost of senior debt already reflects the value of the implied support of being too big, or otherwise systemically important, to be allowed to fail. The risk that deposits might be exposed to loss is even more remote partly due to deposit insurance but, possibly more importantly, because they are deeply insulated from risk by the substantial layers of equity and junior ranking liabilities that must be exhausted before assets are insufficient to cover deposit liabilities.

To what extent would the public sector continue to stand behind the banking system once the proposed level of self insurance is in place?

Assuming the market capacity constraint question could be addressed (which I think it can), the solution that APRA has proposed seems to me to give the official family much greater options for dealing with future banking crises without having to call on the taxpayer to underwrite the risk of recapitalising failed or otherwise non-viable banks.

It does not, however, eliminate the need for liquidity support. I know some people argue that this is a distinction without a difference but I disagree. The reality is that banking systems built on mostly illiquid assets will likely face future crises of confidence where the support of the central bank will be necessary to keep the financial wheels of the economy turning.

There are alternative ways to construct a banking system. Mervyn King, for example, has advocated a version of the Chicago Plan under which all bank deposits must be 100% backed by liquid reserves that would be limited to safe assets such as government securities or reserves held with the central bank. Until we decide to go down that path, or something similar, the current system requires the central bank to be the lender of last resort. That support is extremely valuable and is another design feature that sets banks apart from other companies. It is not the same however, as bailing out a bank via a recapitalisation.

Conclusion

I have been sitting on this post for a few weeks while trying to consider the pros and cons. As always, the risk remains that I am missing something. That said, this looks to me like a necessary (and I would argue desirable) enhancement to the Australian financial system that not only underpins its safety and stability but also takes us much closer to a level playing field. Big banks will always have the advantage of sophistication, scale and efficiency that comes with size but any funding cost advantage associated with being too big to fail now looks to be priced into the cost of the additional layers of loss absorption this proposal would require them to put in place.

Tony