“Debt and institutions dealing with debt have two faces: a quiet one and a tumultuous one …. The shift from an information-insensitive state where liquidity and trust prevails because few questions need to be asked, to an information-sensitive state where there is a loss of confidence and a panic may break out is part of the overall system: the calamity is a consequence of the quiet. This does not mean that one should give up on improving the system. But in making changes, it is important not to let the recent crisis dominate the new designs. The quiet, liquid state is hugely valuable.”

Bengt Holmstrom (2015)

The quote above comes from an interesting paper by Bengt Holmstrom that explores the ways in which the role money markets play in the financial system is fundamentally different from that played by stock markets. That may seem like a statement of the obvious but Holmstrom argues that some reforms of credit markets which based on the importance of transparency and detailed disclosure are misconceived because they do not reflect these fundamental differences in function and mode of operation.

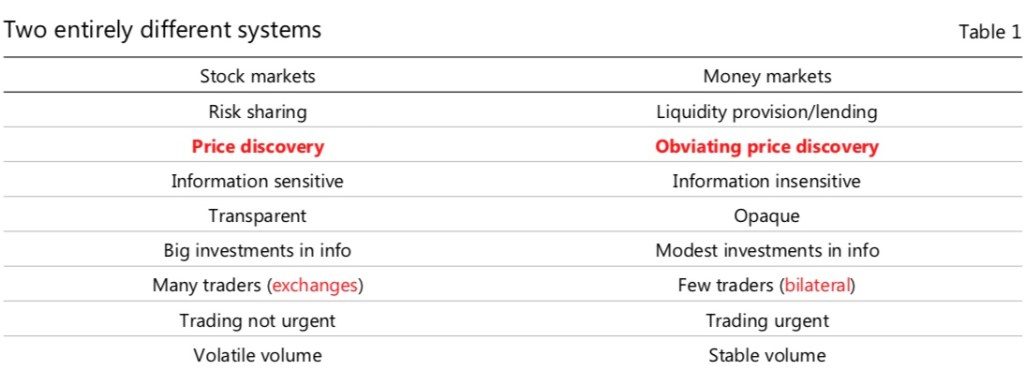

Holmstrom argues that the focus and purpose of stock markets is price discovery for the purpose of allocating risk efficiently. Money markets, in contrast are about obviating the need for price discovery in order to enhance the liquidity of the market. Over-collateralisation is one of the features of the money market that enable deep, liquid trading to occur without the need to understand the underlying risk of the assets that are being funded .

“The design of money market policies and regulations should recognise that money markets are very different from stock markets. Lessons from the latter rarely apply to the former, because markets for risk-sharing and markets for funding have their own separate logic. The result is two coherent systems with practices that are in almost every respect polar opposites.”

From “Understanding the role of debt in the financial system” Bengt Holmstrom (BIS Working Papers No 479 – January 2015)

Holmstrom appears to have written the paper in response to what he believes are misconceived attempts to reform credit markets in the wake of the recent financial crisis. These reforms have often drawn on insights grounded in our understanding of stock markets where information and transparency are key requirements for efficient price discovery and risk management. His paper presents a perspective on the logic of credit markets and the structure of debt contracts that highlights the information insensitivity of debt. This perspective explains among other things why he believes that information insensitivity is the natural and desired state of the money markets.

Holmstrom notes that one of the puzzles of the GFC was how people traded so many opaque instruments with a seeming ignorance of their real risk. There is a tendency to see this as a conspiracy by bankers to confuse and defraud customers which in turn has prompted calls to make money market instruments more transparent. While transparency and disclosure is essential for risk pricing and allocation, Holmstrom argues that this is not the answer for money markets because they operate on different principles and serve a different function.

“I will argue that a state of “no questions asked” is the hallmark of money market liquidity; that this is the way money markets are supposed to look when they are functioning well.”

“Among economists, the mistake is to apply to money markets the lessons and logic of stock markets.”

“The key point I want to communicate today is that these two markets are built on two entirely different, one could say diametrically opposite, logics. Ultimately, this is because they serve two very different purposes. Stock markets are in the first instance aimed at sharing and allocating aggregate risk. To do that effectively requires a market that is good at price discovery.

“But the logic behind transparency in stock markets does not apply to money markets. The purpose of money markets is to provide liquidity for individuals and firms. The cheapest way to do so is by using over-collateralised debt that obviates the need for price discovery. Without the need for price discovery the need for public transparency is much less. Opacity is a natural feature of money markets and can in some instances enhance liquidity, as I will argue later.”

“Why does this matter? It matters because a wrong diagnosis of a problem is a bad starting point for remedies. We have learned quite a bit from this crisis and we will learn more. There are things that need to be fixed. But to minimise the chance of new, perhaps worse mistakes, we need to analyse remedies based on the purpose of liquidity provision. In particular, the very old logic of collateralised debt and the natural, but sometimes surprising implications this has for how information and risk are handled in money markets, need to be properly appreciated.”

There is a section of the paper titled “purposeful opacity” which, if I understood him correctly, seemed to extend his thesis on the value of being able to trade on an “information insensitive” basis to argue that “opacity” in the debt market is something to be embraced rather than eliminated. I struggled with embracing opacity in this way but that in no way diminishes the validity of the distinction he draws between debt and equity markets.

The other useful insight was the way in which over-collateralistion (whether explicit or implicit) anchors the liquidity of the money market. His discussion of why the sudden transition from a state in which the creditworthiness of a money market counter-party is taken for granted to one in which doubt emerges also rings true.

The remainder of this post mostly comprises extracts from the paper that offer more detail on the point I have summarised above. The paper is a technical one but worth the effort for anyone interested in the question of how banks should finance themselves and the role of debt in the financial system.

Money markets versus stock markets

Holmstrom argues that each system displays a coherent internal logic that reflects its purpose but these purposes are in many respects polar opposites.

Stock markets are primarily about risk sharing and price discovery. As a consequence, these markets are sensitive to information and value transparency. Traders are willing to make substantial investments to obtain this information. Liquidity is valuable but equity investors will tend to trade less often and in lower volumes than debt markets.

Money markets, in contrast, Holmstrom argues are primarily about liquidity provision and lending. The price discovery process is much simpler but trading is much higher volume and more urgent.

“The purpose of money markets is to provide liquidity. Money markets trade in debt claims that are backed, explicitly or implicitly, by collateral.

“People often assume that liquidity requires transparency, but this is a misunderstanding. What is required for liquidity is symmetric information about the payoff of the security that is being traded so that adverse selection does not impair the market. Without symmetric information adverse selection may prevent trade from taking place or in other ways impair the market (Akerlof (1970)).”

“Trading in debt that is sufficiently over-collateralised is a cheap way to avoid adverse selection. When both parties know that there is enough collateral, more precise private information about the collateral becomes irrelevant and will not impair liquidity.”

The main purpose of stock markets is to share and allocate risk … Over time, stock markets have come to serve other objectives too, most notably governance objectives, but the pricing of shares is still firmly based on the cost of systemic risk (or a larger number of factors that cannot be diversified). Discovering the price of systemic risk requires markets to be transparent so that they can aggregate information efficiently.

Purposeful opacity

“Because debt is information-insensitive … traders have muted incentives to invest in information about debt. This helps to explain why few questions were asked about highly rated debt: the likelihood of default was perceived to be low and the value of private information correspondingly small.”

Panics: The ill consequences of debt and opacity

“Over-collateralised debt, short debt maturities, reference pricing, coarse ratings, opacity and “symmetric ignorance” all make sense in good times and contribute to the liquidity of money markets. But there is a downside. Everything that adds to liquidity in good times pushes risk into the tail. If the underlying collateral gets impaired and the prevailing trust is broken, the consequences may be cataclysmic”

“The occurrence of panics supports the informational thesis that is being put forward here. Panics always involve debt. Panics happen when information-insensitive debt (or banks) turns into information-sensitive debt … A regime shift occurs from a state where no one feels the need to ask detailed questions, to a state where there is enough uncertainty that some of the investors begin to ask questions about the underlying collateral and others get concerned about the possibility”

These events are cataclysmic precisely because the liquidity of debt rested on over-collateralisation and trust rather than a precise evaluation of values. Investors are suddenly in the position of equity holders looking for information, but without a market for price discovery. Private information becomes relevant, shattering the shared understanding and beliefs on which liquidity rested (see Morris and Shin (2012) for the general mechanism and Goldstein and Pauzner (2005) for an application to bank runs).

Would transparency have helped contain the contagion?

“A strong believer in the informational efficiency of markets would argue that, once trading in credit default swaps (CDS) and then the ABX index began, there was a liquid market in which bets could be made both ways. The market would find the price of systemic risk based on the best available evidence and that would serve as a warning of an imminent crisis. Pricing of specific default swaps might even impose market discipline on the issuers of the underlying debt instruments”

Shadow banking

“The rapid growth of shadow banking and the use of complex structured products have been seen as one of the main causes of the financial crisis. It is true that the problems started in the shadow banking system. But before we jump to the conclusion that shadow banking was based on unsound, even shady business practices, it is important to try to understand its remarkable expansion. Wall Street has a hard time surviving on products that provide little economic value. So what drove the demand for the new products?”

“It is widely believed that the global savings glut played a key role. Money from less developed countries, especially Asia, flowed into the United States, because the US financial system was perceived to be safe … More importantly, the United States had a sophisticated securitisation technology that could activate and make better use of collateral … Unlike the traditional banking system, which kept mortgages on the banks’ books until maturity, funding them with deposits that grew slowly, the shadow banking system was highly scalable. It was designed to manufacture, aggregate and move large amounts of high-quality collateral long distances to reach distant, sizable pools of funds, including funds from abroad.”

“Looking at it in reverse, the shadow banking system had the means to create a lot of “parking space” for foreign money. Securitisation can manufacture large amounts of AAA-rated securities provided there is readily available raw material, that is, assets that one can pool and tranche”

“I am suggesting that it was an efficient transportation network for collateral that was instrumental in meeting the global demand for safe parking space.”

“The distribution of debt tranches throughout the system, sliced and diced along the way, allowing contingent use of collateral”

“Collateral has been called the cash of shadow banking (European repo council (2014)). It is used to secure large deposits as well as a host of derivative transactions such as credit and interest rate swaps.”

There is a relatively recent, but rapidly growing, body of theoretical research on financial markets where the role of collateral is explicitly modelled and where the distinction between local and global collateral is important

“Viewed through this theoretical lens, the rise of shadow banking makes perfectly good sense. It expanded in response to the global demand for safe assets. It improved on traditional banking by making collateral contingent on need and allowing it to circulate faster and attract more distant capital. In addition, securitisation created collateral of higher quality (until the crisis, that is) making it more widely acceptable. When the crisis hit, bailouts by the government, which many decry, were inevitable. But as just discussed, the theory supports the view that bailouts were efficient even as an ex ante policy (if one ignores potential moral hazard problems). Exchanging impaired collateral for high-quality government collateral, as has happened in the current crisis (as well as historically with clearing houses), can be rationalised on these grounds.”

Some policy implications

A crisis ends only when confidence returns. This requires getting back to the no-questions-asked state ….

Transparency would likely have made the situation worse

“By now, the methods out of a crisis appear relatively well understood. Government funds need to be committed in force (Geithner (2014)). Recapitalisation is the only sensible way out of a crisis. But it is much less clear how the banking system, and especially shadow banking, should be regulated to reduce the chance of crisis in the first place. The evidence from the past panic suggests that greater transparency may not be that helpful.”

“The logic of over-capitalisation in money markets leads me to believe that higher capital requirements and regular stress tests is the best road for now.”

“Transparency can provide some market discipline and give early warning of trouble for individual banks. But it may also lead to strategic behaviour by management. The question of market discipline is thorny. In good times market discipline is likely to work well. The chance that a bank that is deemed risky would trigger a panic is non-existent and so the bank should pay the price for its imprudence. In bad times the situation is different. The failure of a bank could trigger a panic. In bad times it would seem prudent to be less transparent with the stress tests (for some evidence in support of this dichotomy, see Machiavelli (1532)).”