Given the central role that money plays in our economy, understanding how the rise of digital money will play out is becoming increasingly important. There is a lot being written on this topic but today’s post is simply intended to flag a paper titled “The Rise of Digital Money” that is one of the more useful pieces of analysis that I have come across. The paper is not overly long (20 pages) but the authors (Tobias Adrian and Tommaso Mancini-Griffoli) have also published a short summary of the paper here on the VOX website maintained by the Centre for Economic Policy Research.

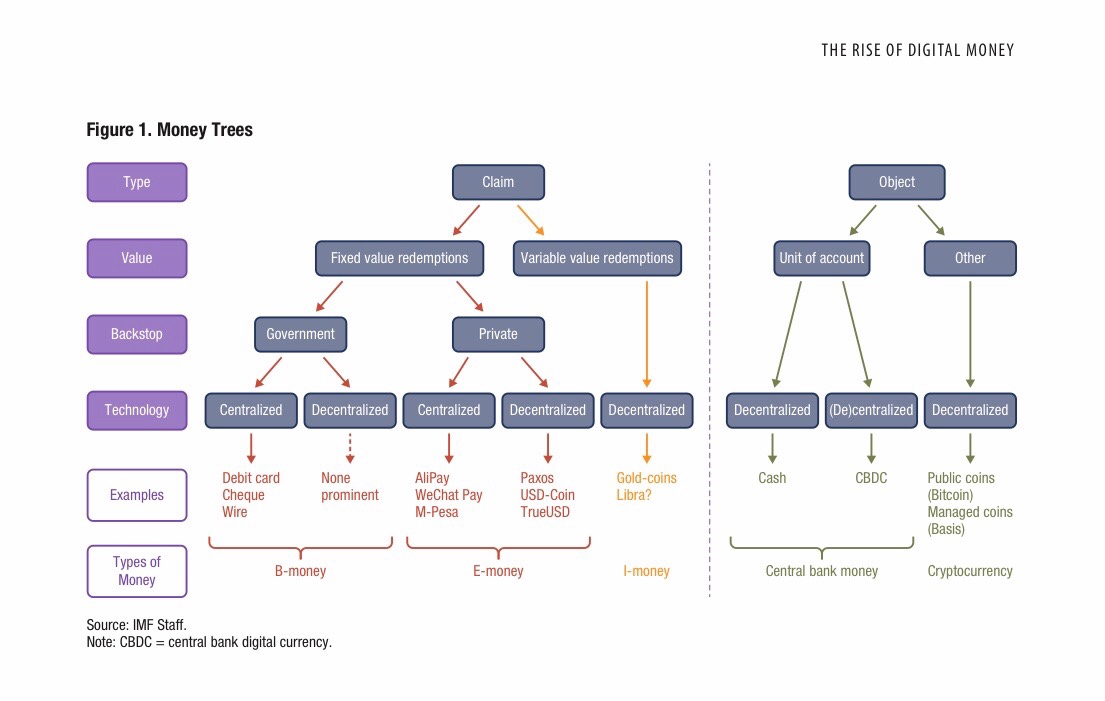

Part of the problem with thinking about the rise of digital money is being clear about how to classify the various forms. The authors offer the following framework that they refer to as a Money Tree.

This taxonomy identifies four key features that distinguish the various types of money (physical and digital):

- Type – is it a “claim” or an “object”?

- Value – is it the “unit of account” employed in the financial system, a fixed value in that unit of account, or a variable value?

- Backstop – if there is a fixed value redemption, is that value “backstopped” by the government or does it rely solely on private mechanisms to support the fixed exchange rate?

- Technology – centralised or decentralised?

Using this framework, the authors discuss the rise of stablecoins

“Adoption of new forms of money will depend on their attractiveness as a store of value and means of payment. Cash fares well on the first count, and bank deposits on both. So why hold stablecoins? Why are stablecoins taking off? Why did USD Coin recently launch in 85 countries,1 Facebook invest heavily in Libra, and centralised variants of the stablecoin business model become so widespread? Consider that 90% of Kenyans over the age of 14 use M-Pesa and the value of Alipay and WeChat Pay transactions in China surpasses that of Visa and Mastercard worldwide combined.

The question is all the more intriguing as stablecoins are not an especially stable store of value. As discussed, they are a claim on a private institution whose viability could prevent it from honouring its pledge to redeem coins at face value. Stablecoin providers must generate trust through the prudent and transparent management of safe and liquid assets, as well as sound legal structures. In a way, this class of stablecoins is akin to constant net asset value funds which can break the buck – i.e. pay out less than their face value – as we found out during the global financial crisis.

However, the strength of stablecoins is their attractiveness as a means of payment. Low costs, global reach, and speed are all huge potential benefits. Also, stablecoins could allow seamless payments of blockchain-based assets and can be embedded into digital applications by an active developer community given their open architecture, as opposed to the proprietary legacy systems of banks.

And, in many countries, stablecoins may be issued by firms benefitting from greater public trust than banks. Several of these advantages exist even when compared to cutting-edge payment solutions offered by banks called fast-payments.2

But the real enticement comes from the networks that promise to make transacting as easy as using social media. Economists beware: payments are not the mere act of extinguishing a debt. They are a fundamentally social experience tying people together. Stablecoins are better integrated into our digital lives and designed by firms that live and breathe user-centric design.

And they may be issued by large technology firms that already benefit from enormous global user bases over which new payment services could spread like wildfire. Network effects – the gains to a new user growing exponentially with the number of users – can be staggering. Take WhatsApp, for instance, which grew to nearly 2 billion users in ten years without any advertisement, based only on word of mouth!”

“The rise of digital currency”, Tobias Adrian, Tommaso Mancini-Griffoli 09 September 2019 – Vox CEPR Policy Portal

The authors then list the risks associated with the rise of stablecoins:

- The potential disintermediation of banks

- The rise of new monopolies

- The threat to weak currencies

- The potential to offer new opportunities for money laundering and terrorist financing

- Loss of “seignorage” revenue

- Consumer protection and financial stability

These risks are not dealt with in much detail. The potential disintermediation of banks gets the most attention (the 20 page paper explores 3 scenarios for how the disintermediation risk might play out).

The authors conclude with a discussion of what role central banks play in the rise of digital currency. They note that many central banks are exploring the desirability of stepping into the game and developing a Central Bank Digital Currency (CBDC) but do not attempt to address the broader question of whether the overall idea of a CBDC is a good one. They do however explore how central banks could work with stablecoin providers to develop a “synthetic” form of central bank digital currency by requiring the “coins” to be backed with central bank reserves.

This is effectively bringing the disrupters into the fold by turning them into a “narrow bank”. Izabella Kaminska (FT Alphaville) has also written an article on the same issue here that is engagingly titled “Why dealing with fintechs is a bit like dealing with pirates”.

The merits of narrow banking lie outside the scope of this post but it a topic with a very rich history (search on the term “Chicago Plan”) and one that has received renewed support in the wake of the GFC. Mervyn King (who headed the Bank of England during the GFC), for example, is one prominent advocate.

Hopefully you found this useful, if not my summary then at least the links to some articles that have helped me think through some of the issues.

Tony

Now that is interesting. Quite aligned to my thinking on the topic and I thought I was being simplistic

LikeLike

Like!! Great article post.Really thank you! Really Cool.

LikeLike