… is the title of an interesting paper by Gary Gorton and Jeffrey Zhang which argues that:

- Cryptocurrency, or stablecoins to be more precise, can be viewed as the latest variation in a long history of privately produced money

- The experience of the United States during the Free Banking Era of the 19th century suggests that ” … privately produced monies are not an effective medium of exchange because they are not always accepted at par and are subject to bank runs”

- Stablecoins are not as yet a systemic issue but could be, so policymakers need to adjust the regulatory framework now to be ready as these new forms of private money grow and and potentially evolve into something that can’t be ignored

- Policy responses include regulating stablecoin issuers as banks and issuing a central bank digital currency

So what?

I am not convinced that a central bank digital currency is the solution. I can see a case for greater regulation of stablecoins but you need to be clear about exactly what type of stablecoin requires a policy response. Gorton and Zhang distinguish three categories …

The first includes cryptocurrencies that are not backed by anything, like Bitcoin. We call these “fiat cryptocurrencies.” Their defining feature is that they have no intrinsic value. Second, there are specialized “utility coins,” like the JPMorgan coin that is limited to internal use with large clients. Finally, there are “stablecoins,” which aspire to be used as a form of private money and so are allegedly backed one-for-one with government fiat currency (e.g., U.S. dollars)

I am yet to see a completely satisfactory taxonomy of stablecoins but at a minimum I would break the third category down further to distinguish the ways in which the peg is maintained. The (relatively few?) stablecoins that actually hold high quality USD assets on a 1:1 basis are different from those which hold material amounts of commercial paper in their reserve asset pool and different again from those which employ algorithmic protocols to maintain the peg.

However, you do not necessarily have to agree with their taxonomy, assessments or policy suggestions to get value from the paper – three things I found useful and interesting:

- The “no-questions-asked ” principle for anything that functions or aims to function as money

- Some technical insights into the economic and legal properties of stablecoins and stablecoin issuers

- Lessons to be learned from history, in particular the Free Banking Era of the 19th century

The “no-questions-asked” principle.

Money is conventionally defined in terms of three properties; a store of value, a unit of account and a medium of exchange. Gorton and Zhang argue that “The property that’s most obvious, yet not explicitly presented, is that money also must satisfy the no-questions-asked (“NQA”) principle, which requires the money be accepted in a transaction without due diligence on its value“. They freely admit that they have borrowed this idea from Bengt Holmstrom though I think he actually uses the term “information insensitive” as opposed to the more colloquial NQA principle.

Previous posts on this blog have looked at both Holmstrom’s paper and other work that Gorton has co-authored on the optimal level of information that different types of bank stakeholders require. If I understood Holmstrom correctly, he seemed to extend his thesis on the value of being able to trade on an “information insensitive” basis to argue that “opacity” in the debt market is something to be embraced rather than eliminated. I struggle with embracing opacity in this way but that in no way diminishes the validity of the distinction he draws between the relative value of information in debt and equity markets and its impact on liquidity.

Gorton and Zhang emphasise the importance of deposit insurance in underwriting confidence in and the liquidity of bank deposits as the primary form of private money. I think that is true in the sense that most bank deposit holders do not understand the mechanics of the preferred claim they have on the assets of the bank they have lent to but it seems to me that over-collateralisation is equally as important in underwriting the economics of bank deposits.

If I have not lost you at this point, you can explore this question further via this link to a post I did titled “Bank deposits – turning unsecured loans to highly leveraged companies into (mostly) risk free assets – an Australian perspective“. From my perspective, the idea that any form of money has to be designed to be “information insensitive” or NQA rings very true.

Insights drawn from a technical analysis of stablecoins and stablecoin issuers.

The paper delves in a reasonable amount of detail into the technicalities of whether stablecoins are economically or legally equivalent to demand deposits and the related question of whether stablecoin issuers might be considered to be banks. The distinction between the economic and the legal status is I think especially useful for understanding how banking regulators might engage with the stablecoin challenge.

The over arching point is that stablecoins that look and function like bank demand deposits should face equivalent levels of regulation. That does not necessarily mean exactly the same set of rules but something functionally equivalent.

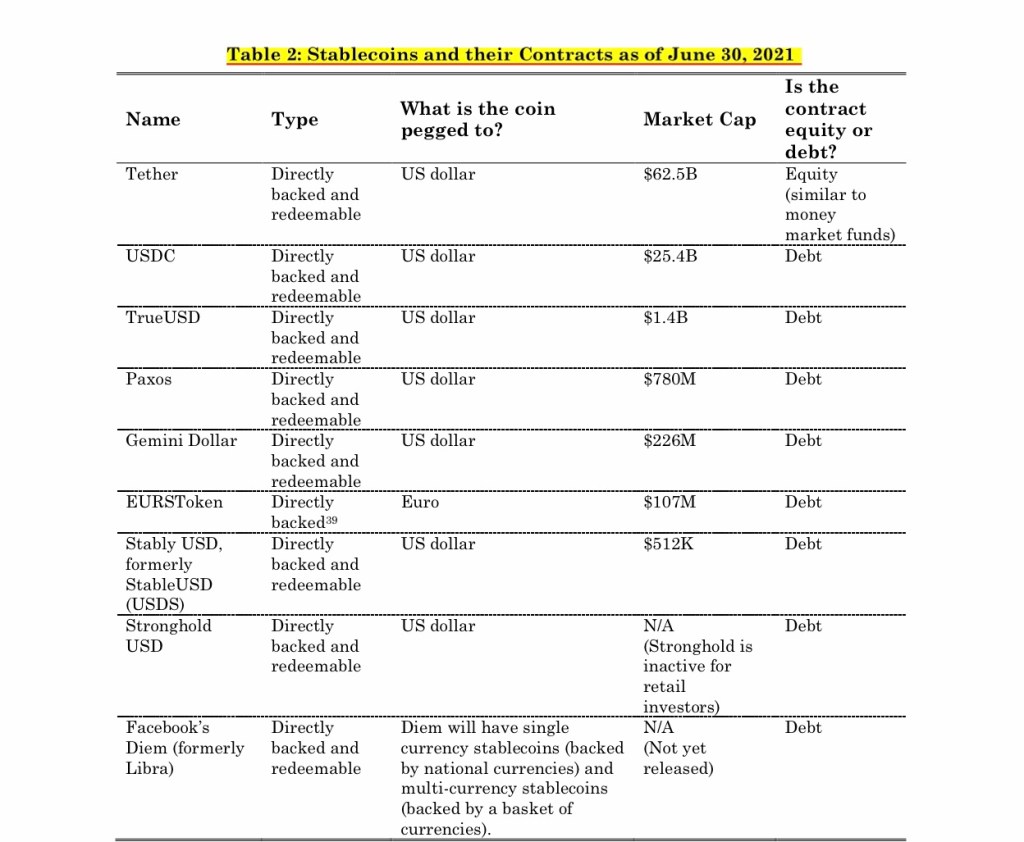

One practical outcome of this analysis that I had not considered previously is that they deem Tether to be based on an “equity contract” relationship with its users whereas the other stablecoins they analyse are “debt contracts” (see below). The link between Tether and a money market fund and the risk of “breaking the buck” has been widely canvassed but I had not previously seen the issue framed in these legal terms.

This technical analysis is summarised in two tables (Table 2: Stablecoins and their Contracts as of June 30, 2021 and Table 3: Stablecoins, Redemptions, and Fiat Money as of June 30. 2021) that offer a useful reference point for understanding the mechanics and details of some of the major stablecoins issued to date. In addition, the appendix to the paper offers links to the sources used in the tables.

Lessons to be learned from history

It may have been repeated to the point of cliche but the idea that “those who cannot remember the past are condemned to repeat it” (George Santayana generally gets the credit for this but variations are attributed to Edmund Burke and Sir Winston Churchill) resonates strongly with me. The general argument proposed by Gorton and Zhang is that lots of the ideas being tried out in stablecoin design and DeFi are variations on general principles that were similarly employed in the lightly regulated Free Banking Era but found wanting.

Even if you disagree with the conclusions they draw, the general principle of using economic history to explore what can be learned and what mistakes to avoid remains a useful discipline for any practitioner of the dark arts of banking and money creation.

Summing up in the authors’ own words

The paper is long (41 pages excluding the Appendix) but I will wrap up this post with an extract that gives you the essence of their argument in their own words.

Tony – From the Outside

Conclusion

The more things change, the more they stay the same. It is still the case that regulation is being outpaced by innovation—thereby creating an uneven playing field—as it is easier and cheaper for more technologically advanced firms to offer similar products and services.

In this case, it is also true that the problems associated with privately produced money are the same as they were one hundred and fifty years ago. We stress three points from our review of history. First, the use of private bank notes was a failure because they did not satisfy the NQA principle. Second, the U.S. government took control of the monetary system under the National Bank Act and subsequent legislation in order to eliminate the private bank note system in favor of a uniform currency—namely, national bank notes. Third, runs on demand deposits only ended with deposit insurance in 1934.

Currently, it does not appear that stablecoins are used as money. But, as stablecoins evolve further, the stablecoin world will look increasingly like an unregulated version of the Free Banking Era—a world of wildcat banking. During the Free Banking Era, private bank monies circulated at time-varying discounts based on geography and the perceived risk of the issuing bank. Stablecoin prices are independent of geography but not independent of the perceived risk of their backing assets. If they succeed in differentiating themselves from fiat cryptocurrencies and become used as money, then they will likely trade at time-varying discounts as well. Policymakers have a couple of ways to address this development, and they better get going.

2 thoughts on “Taming wildcat stablecoins …”