Matt Levine’s Money Stuff column (Bloomberg Opinion) had a great piece today which, while nominally focussed on the enduring question of “Looking for Tether’s Money”, is worth reading for the neat summary he offers of how finance turns risky assets into safe assets. The column is behind a paywall but you can access it for free by signing up for his daily newsletter.

This particular piece of the magic of finance is of course achieved by dividing up claims on risky assets into tranches with differing levels of seniority. In Matt’s words…

Most of what happens in finance is some form of this move. And the reason for that is basically that some people want to own safe things, because they have money that they don’t want to lose, and other people want to own risky things, because they have money that they want to turn into more money. If you have something that is moderately risky, someone will buy it, but if you slice it into things that are super safe and things that are super risky, more people might buy them. Financial theory suggests that this is impossible but virtually all of financial practice disagrees.

Money Stuff, Matt Levine Bloomberg, 7 October 2021

Matt also offers a neat description of how this works in banking

A bank makes a bunch of loans in exchange for senior claims on businesses, houses, etc. Then it pools those loans together on its balance sheet and issues a bunch of different claims on them. The most senior claims, classically, are “bank deposits”; the most junior claims are “equity” or “capital.” Some people want to own a bank; they think that First Bank of X is good at running its business and will grow its assets and improve its margins and its stock will be worth more in the future, so they buy equity (shares of stock) of the bank. Other people, though, just want to keep their money safe; they put their deposits in the First Bank of X because they are confident that a dollar deposited in an account there will always be worth a dollar.

The fundamental reason for this confidence is that bank deposits are senior claims (deposits) on a pool of senior claims (loans) on a diversified set of good assets (businesses, houses). (In modern banking there are other reasons — deposit insurance, etc. — but this is the fundamental reason.) But notice that this is magic: At one end of the process you have risky businesses, at the other end of the process you have perfectly safe dollars. Again, this is due in part to deposit insurance and regulation and lenders of last resort, but it is due mainly to the magic of composing senior claims on senior claims. You use seniority to turn risky things into safe things

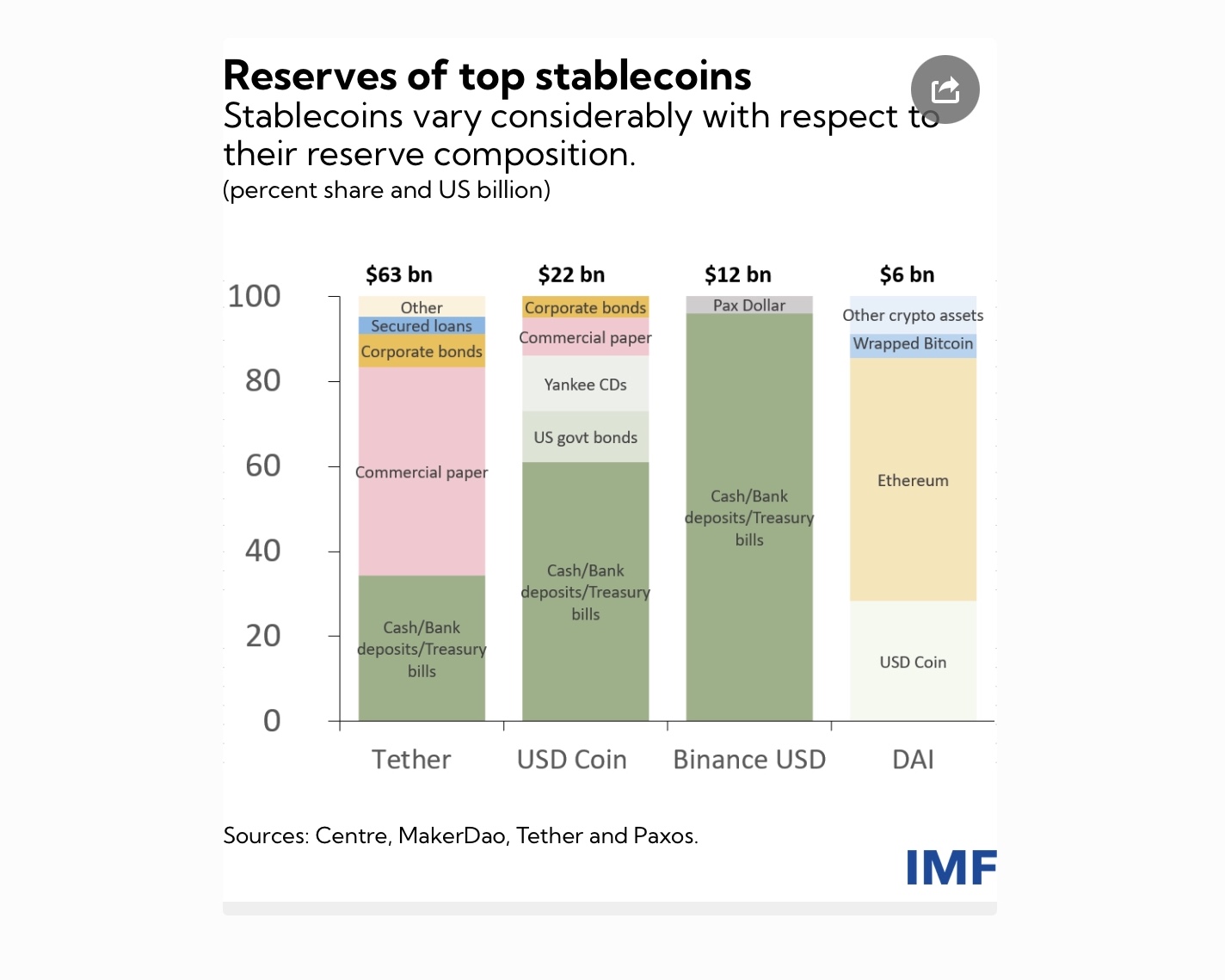

He then applies these principles to the alternative financial world that has been created around crypto assets to explore how the same factors drive both the need/demand for stablecoins and the ways in which crypto finance can meet the demand for safe assets (well “safer” at least).

The one part of his explanation I would take issue with is that he could have delved deeper into the question of whether crypto users require stablecoins to exhibit the same level of risk free exchangeability that we expect of bank deposits in the conventional financial world.

Matt writes…

The people who live in Bitcoin world are people like anyone else. Some of them (quite a lot of them by all accounts) want lots of risk: They are there to gamble; their goal is to increase their money as much as possible. Bitcoin is volatile, but levered Bitcoin is even more volatile, and volatility is what they want.

Others want no risk. They want to put their money into a thing worth a dollar, and be sure that no matter what they’ll get their dollar back. But they don’t want to do that in a bank account or whatever, because they want their dollar to live in crypto world. What they want is a “stablecoin”: A thing that lives on the blockchain, is easily exchangeable for Bitcoin (or other crypto assets) using the tools and exchanges and brokerages and processes of crypto world, but is always worth a dollar

The label “stable” is a relative term so it is not obvious to me that people operating in the crypto financial asset world all necessarily want the absolute certainty of a coin that always trade at par value to the underlying fiat currency. Maybe they do but maybe some are happy with something that is stable enough to do the job of allowing them to do the exchanges they want to do in risky crypto assets. Certainly they already face other costs like gas fees when they trade so maybe something that trades within an acceptable range of par value is good enough?

What it comes down to is first defining exactly what kind of promise the stablecoin backer is making before we start down the path of defining exactly how that promise should be regulated. I do think that the future of stablecoins is likely to be more regulated and that is likely to be a net positive outcome. The term “stablecoin” however encompasses a wide variety of structures and intended uses. The right kind of regulation will be designed with these differences in mind. That said, some of the stablecoin issuers have not done themselves any favours in the loose ways in which they have defined their promise.

Matt’s column is well worth reading if you can access it but the brief outline above flags some of the key ideas and the issues that I took away. The ways in which seniority in the loss hierarchy creates safety (or what Gary Gorton refers to as “information insensitivity”) is I think the key insight. I frequently encounter papers and articles discussing the role of bank deposits as the primary form of money in developed economies. These nearly always mention prudential regulation, supervision and deposit insurance but the role of deposit preference is often overlooked. For anyone looking to dig a bit deeper, I did a post here offering an Australian perspective on how this works.

Tony – From the Outside