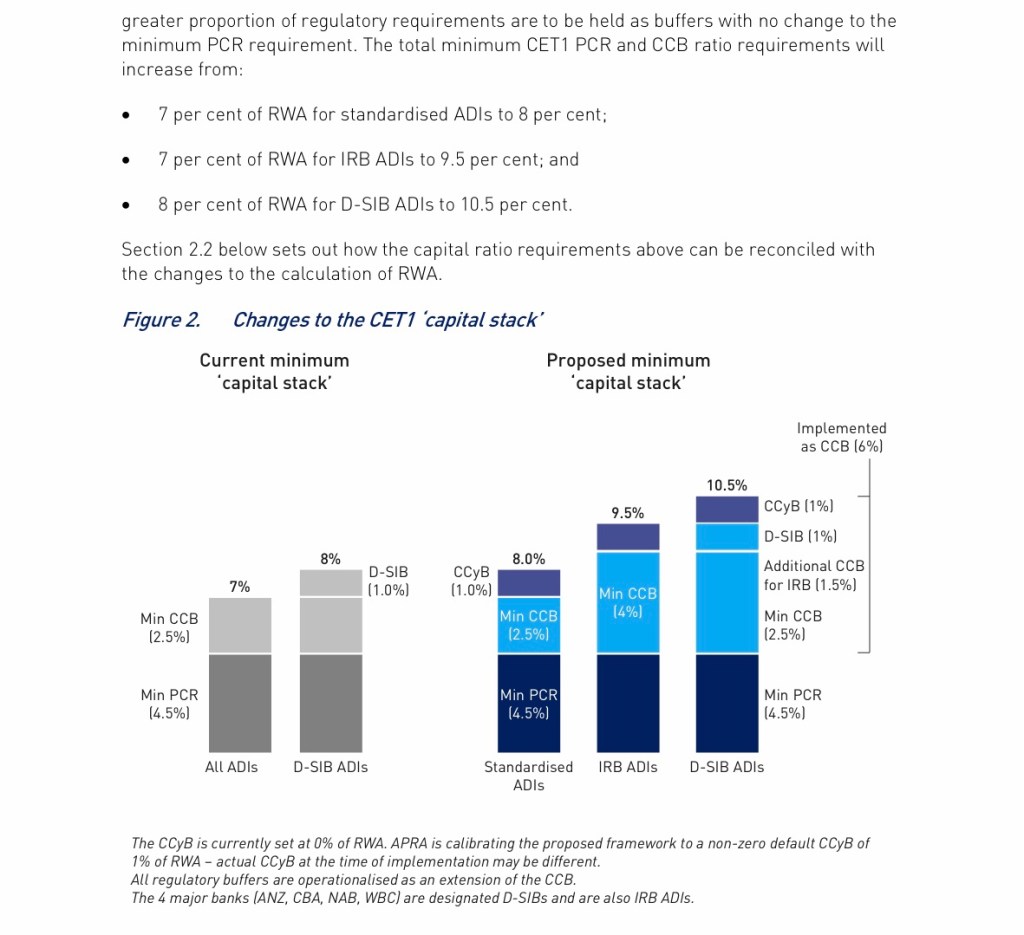

The European Central Bank recently (April 2021) released a report documenting what had been identified in a “Targeted Review of Internal Models”(TRIM). The TRIM Report has lots of interesting information for subject matter experts working on risk models.

It also has one item of broader interest for anyone interested in understanding what it means for an Australian Authorised Deposit Taking Institution (ADI) to be “Unquestionably Strong” per the recommendation handed down by the Australian Financial System Inquiry in 2014 and progressively being enshrined in capital regulation by the Australian Prudential Regulation Authority (APRA).

The Report disclosed that the TRIM has resulted in 253 supervisory decisions that are expected to result in a 12% increase in the aggregate RWAs of the models covered by the review. European banks may not be especially interested in the capital adequacy of their Australian peers but international peer comparisons have become one of the core lens through which Australian capital adequacy is assessed as a result of the FSI recommendation.

There are various ways in which the Unquestionably Strong benchmark is interpreted but one is the requirement that the Australian ADIs maintain a CET1 ratio that lies in the top quartile of international peer banks. A chart showing how Australian ADIs compare to their international peer group is a regular feature of the capital adequacy data they disclose. The changes being implemented by the ECB in response to the TRIM are likely (all other things being equal) to make the Australian ADIs look even better in relative terms in the future.

More detail …

The ECB report documents work that was initiated in 2016 covering 200 on-site model investigations (credit, market and counterparty credit risk) across 65 Significant Institutions (SI) supervised by ECB under what is known as the Single Supervisory Mechanism and extends to 129 pages. I must confess I have only read the Executive Summary (7 pages) thus far but I think students of the dark art of bank capital adequacy will find some useful nuggets of information.

Firstly, the Report confirms that there has been, as suspected, areas in which the outputs of the Internal Models used by these SI varied due to inconsistent interpretations of the BCBS and ECB guidance on how the models should be used to generate consistent and comparable risk measures. This was not however simply due to evil banks seeking to game the system. The ECB identified a variety of areas in which their requirements were not well specified or where national authorities had pursued inconsistent interpretations of the BCBS/ECB requirements. So one of the key outcomes of the TRIM is enhanced guidance from the ECB which it believes will reduce the instances of variation in RWA due to differences in interpretation of what is required.

Secondly the ECB also identified instances in which the models were likely to be unreliable due to a lack of data. As you would expect, this was an issue for Low Default Portfolios in general and Loss Given Default models in particular. As a result, the ECB is applying “limitations” on some models to ensure that the outputs are sufficient to cover the risk of the relevant portfolios.

Thirdly the Report disclosed that the TRIM has resulted in 253 supervisory decisions that are expected to result in a 12% increase in the aggregate RWAs of the models covered by the review.

As a follow-up to the TRIM investigations, 253 supervisory decisions have been issued or are in the process of being issued. Out of this total, 74% contain at least one limitation and 30% contain an approval of a material model change. It is estimated that the aggregated impact of TRIM limitations and model changes approved as part of TRIM investigations will lead to a 12% increase in the aggregated RWA covered by the models assessed in the respective TRIM investigations. This corresponds to an overall absolute increase in RWA of about €275 billion as a consequence of TRIM and to a median impact of -51 basis points and an average impact of -71 basis points on the CET1 ratios of the in-scope institutions.

European Central Bank, “Targeted Review of Internal Models – Project Report”, April 2021, (page 7)

Summing up

Interest in this report is obviously likely to be confined for the most part to the technical experts that labour in the bowels of the risk management machines operated by the large sophisticated banks that are accredited to measure their capital requirements using internal models. There is however one item of general interest to an Australian audience and that is the news that the RWA of their European peer banks is likely to increase by a material amount due to modelling changes.

It might not be obvious why that is so for readers located outside Australia. The reason lies in the requirement that our banks (or Authorised Deposit-Taking Institutions to use the Australian jargon) be capitalised to an “Unquestionably Strong” level.

There are various ways in which this benchmark is interpreted but one is the requirement that the Australian ADIs maintain a CET1 ratio that lies in the top quartile of international peer banks. A chart showing how Australian ADIs compare to this international peer group is a regular feature of the capital adequacy data disclosed by the ADIs and the changes being implemented by the ECB are likely (all other things being equal) to make the Australian ADIs look even better in relative terms in the future.

Tony – From the Outside