Interesting post by Marc Rubinstein on the history of clearing houses and Sam Bankman-Fried’s proposal for a new approach.

— Read on www.netinterest.co/p/sbf-and-the-future-of-markets-d79

Interesting post by Marc Rubinstein on the history of clearing houses and Sam Bankman-Fried’s proposal for a new approach.

— Read on www.netinterest.co/p/sbf-and-the-future-of-markets-d79

My last post looked at a RBNZ consultation paper which addressed the question “How much capital is enough?”. The overall quantum of capital the RBNZ arrived at (16% of RWA plus) seemed reasonable but it was less obvious that relying almost entirely on CET1 was the right solution. That prompted me to revisit an earlier consultation paper in which the RBNZ set out its case for why it did not want contingent capital instruments to play a significant role in the capital structure of the banks it supervises. This post explores the arguments the RBNZ marshals to support its position as part of a broader exploration of the debate over what counts as capital.

The traditional approach to this question assumes that common equity is unquestionably the best form of capital from the perspective of loss absorption. Consequently, the extent to which alternative forms of funding count as capital is judged by common equity benchmarks; e.g. the extent to which the funding is a permanent commitment (i.e. no maturity date) and the returns paid to investors depend on the profitability or capacity of the company to pay (failure to pay is not an event of default).

There is no dispute that tangible common equity unquestionably absorbs loss and is the foundation of any company’s capital structure but I believe contingent convertible capital instruments do potentially add something useful to the bank capital management toolkit. I will attempt to make the case that a foundation of common equity, supplemented with some debt that converts to common equity if required, is better than a capital structure comprised solely or largely of common equity.

The essence of my argument is that there is a point in the capital structure where adding contingent convertible instruments enhances market discipline relative to just adding more common equity. The RBNZ discusses the potential value of these structures in their consultation paper:

“49. The theoretical literature on contingent debt explores how these instruments might reduce risk (i.e. lower the probability of insolvency) for an individual bank.

50. Two effects have been identified. Firstly, adding contingent debt to a bank’s balance sheet directly increases the loss absorbing potential of the bank, relative to issuing pure debt (but not relative to acquiring more common equity). This follows directly from the fact that removing the debt is an essential part of every contingent debt instrument. Secondly, depending on the terms, contingent capital may cause bank management to target a lower level of risk (incentive effects). In other words, in theory, a contingent debt instrument both reduces the probability a bank will incur losses and absorbs losses that do eventuate. Because of both these factors, contingent debt is expected, in theory, to reduce the risk of bank failure.

51. Focusing on the second of these effects, management incentives, it matters whether, when the debt is written off, holders are compensated in the form of newly issued shares (“conversion”). If conversion is on such a scale as to threaten existing shareholders with a loss of control of the bank, it will be optimal for bank management to target a lower level of risk exposure for a given set of circumstances than would have been the case otherwise. For example, bank management may be less tolerant of asset volatility, and more likely to issue new equity to existing shareholders, when capital is low rather than risk triggering conversion.”

RBNZ Capital Review Paper 2: What should qualify as bank capital? Issues and Options (para 49 – 51) – Emphasis added

So the RBNZ does recognise the potential value of contingent debt instruments which convert into common equity but chose to downplay the benefits while placing much greater weight on a series of concerns it identified.

Before digging into the detail of the RBNZ concerns, it will be helpful to first clarify terminology. I am using the term Contingent Convertible Instruments for my preferred form of supplementary capital whereas much of the RBNZ paper focuses on what it refers to as “Contingent debt instruments“, which it defines in part as “debt that absorbs loss via write-off, which may or may not be followed by conversion”.

I had not picked this up on my first read of the RBNZ paper but came to realise we are talking slightly at cross purposes. The key words to note are “contingent” and “convertible”.

I had taken it as given that these instruments would be convertible but the RBNZ places more emphasis on the possibility that conversion “may or may not” follow write-off. Small point but worth noting when evaluating the arguments.

The RBNZ understandably focuses on the write-off part of the loss absorption process whereas I focus on conversion because it is essential to preserving a loss hierarchy that allocates losses to common equity in the first instance. If we ignore for a moment the impact of bail-in (either by conversion or write-off), the order in which losses are applied to the various sources of funding employed by a bank follows this loss hierarchy:

Under bail-in, writing off a contingent capital instrument generates an increase in common equity that accrues to the existing ordinary shareholders thereby negating the traditional loss hierarchy that requires common equity to be exhausted before more senior instruments can be required to absorb loss.

Conversion is a far better way to effect loss absorption because ordinary shareholders still bear the brunt of any loss, albeit indirectly via the dilution of their shareholding (and associated share price losses). In theory, conversion shields the AT1 investors from loss absorption because they receive common equity equivalent in value to the book value of their claim on the issuer. In practice, it is less clear that the AT1 investors will be able to sell the shares received at the conversion price or better but they are still better off than if they had simply seen the value of their investment written-off. If you are interested in digging deeper, this post looks at how loss absorption works under bail-in.

The RBNZ does recognise this dynamic but still chose to reject these advantages so it is time to look at their concerns.

The RBNZ identified six concerns to justify its in principle decision to exclude the use of contingent capital instruments in the NZ capital adequacy framework.

I don’t imagine the RBNZ is much concerned with my opinion but I don’t find the first three concerns to be compelling. I set out my reasons later in the post but will focus for the moment on three issues that I think do bear deeper consideration. You do not necessarily have to agree with the RBNZ assessment, or the weight they assign to them, but I believe these concerns must be addressed if we are to make the case for contingent debt.

The RBNZ notes that all New Zealand banks are able to issue a version of contingent debt that qualifies as capital, but that some types of banks may have access to a broader – and cheaper – range of capital opportunities than others. The current definition of capital is thus in part responsible for a somewhat uneven playing field.

The primary concern seems to be banks structured as mutual societies which are unable to issue ordinary shares. They cannot offer contingent debt that includes conversion and must rely on the relatively more expensive option of writing-off of the debt to effect loss absorption.

I think this is a reasonable concern but I also believe there may be ways to deal with it. One option is for these banks to issue Mutual Equity Interests as has been proposed in Australia. Another option (also based on an Australian proposal) is that the increased requirements for loss absorbing capital be confined to the banks which cannot credibly be allowed to fail or be resolved in any other way. I recognise that this option benefits from the existence of deposit insurance which NZ has thus far rejected.

I need to do bit more research on this topic so I plan to revisit the way we deal with small banks, and mutuals in particular, in a future post.

The tax treatment of payments to security holders is one of the basic tests for determining if the security is debt or equity but contingent debt instruments don’t fall neatly into either box. The conversion terms tied to PONV triggers make the instruments equity like when the issuer is under financial stress while the contractual nature of the payments to security holders makes them appear more debt like under normal operating conditions.

I can see a valid prudential concern but only to the extent the debt like features the tax authority relied on in making its determination regarding tax-deductibility somehow undermined the ability of the instrument to absorb loss when required.

There have been instances where securities have been mis-sold to unsophisticated investors (the Monte dei Paschi di Sienna example cited by the RBNZ is a case in point) but it is less obvious that retail investment by itself is sufficient cause to rule out this form of capital.

The only real difference I see over conventional forms of debt is the line where their equity like features come into play. Conventional debt is only ever at risk of loss absorption in the event of bankruptcy where its seniority in the loss hierarchy will determine the extent to which the debt is repaid in full. These new forms of bank capital bring forward the point at which a bank balance sheet can be restructured to address the risk that the restructuring undermines confidence in the bank. The economics of the restructuring are analogous so long as losses are allocated by conversion rather than by write-off alone.

Possibly their core concern is that overseeing instrument compliance is a complex and resource-intensive process that the RBNZ believes does not fit well with its regulatory model that emphasises self-discipline and market discipline. The RBNZ highlights two concerns in particular.

This I think, is the strongest objection the RBNZ raises against contingent debt. Contingent debt securities are clearly more complex than common equity so the RBNZ quite reasonably argues that they need to bring something extra to the table to justify the time, effort and risk associated with them. There is virtually no justification for them if they do, as the RBNZ asserts, work against the principles of self and market discipline that underpin its regulatory philosophy.

The first concern relates to the RBNZ requirement that banks must acknowledge any potential tax implications arising from contingent debt and reflect these potential “tax offsets” in the reported value of capital. Banks are required to obtain a binding ruling from the NZ tax authority (or voluntarily take a tax ”haircut”). The RBNZ acknowledges that a binding ruling can provide comfort that tax is fully accounted for under prudential requirements, but quite reasonably argues that this will only be the case if the ruling that is sought is appropriately specified so as to capture all relevant circumstances.

The RBNZ’s specific concern seems to be what happens when no shares are issued in the event of the contingent loss absorption feature being triggered and hence no consideration is paid to investors in exchange for writing off their debt claim. The bank has made a gain that in principle would create a tax lability but it also seems reasonable to assume that the write off could only occur if the bank was incurring material losses. It follows then that the contingent tax liability created by the write off is highly likely to be set off against the tax losses such that there is no tax to pay.

I am not a tax expert so I may well be missing something but I can’t see a practical risk here. Even in the seemingly unlikely event that there is a tax payment, the money represents a windfall gain for the public purse. That said, I recognise that the reader must still accept my argument regarding the value of having the conversion option to consider it worth dealing with the added complexity.

I and the RBNZ both agree that one of the key planks in the case for accepting contingent debt as bank capital is the beneficial impact on bank risk taking generated by the risk of dilution but the RBNZ argues this beneficial impact is less than it could be when the instrument is issued by a NZ subsidiary to its publicly listed parent.

I may be missing something here but the parent is exposed to dilution if the Non-Viability or Going Concern triggers are hit so I can’t see how that reduces the incentive to control risk unless the suggestion is that NZ management will somehow have the freedom to pursue risky business strategies with no input from their ultimate owners.

The RBNZ cites some statistical evidence that suggests that, in contrast to the experience overseas, there appears to be limited uptake by wholesale investors of contingent debt issued by the big four banks. This prompts them to question whether the terms being offered on instruments issued outside the parent group are not sufficiently attractive for sophisticated investors. This concern seems to be predicated on the view that retail will always be the least sophisticated investors so banks will seek to take advantage of their relative lack of knowledge.

It is arguably true that retail investors will tend be less sophisticated than wholesale investors but that should not in itself lead to the conclusion that any issue targeted at retail is a cynical attempt at exploitation or that retail might legitimately value something differently to the way other investors do. The extent that the structures issued by the Australian parents have thus far concentrated on retail, for example, might equally be explained by the payment of franking credit that was more highly valued by the retail segment. Offshore institutions might also have been negative on the Australian market therefore pushing Australian banks to focus their efforts in the domestic market.

I retain an open mind on this question and need to dig a bit deeper but I don’t see how the fact that retail investment dominates the demand for these structures at a point in time can be construed to be proof that they are being mis-sold.

The reason that the RBNZ rejects the use of these forms of supplementary capital ultimately appears to lie in its regulatory philosophy which is based on the following principles

The RBNZ also acknowledges the value of adopting BCBS consistent standards but this is not a guiding principle. It reserves the right to adapt them to local needs and, in particular, to be more conservative. It should also be noted that the RBNZ has quite deliberately rejected adopting deposit insurance on the grounds (as I understand it) that this encourages moral hazard. They take this a step further by foregoing any depositor preference in the loss hierarchy and by a unique policy of Open Bank Resolution (OBR) under which deposits are explicitly included in the liabilities which can be written down in need to assist in the recapitalisation of an insolvent bank.

In theory, the RBNZ might have embraced contingent convertible instruments on the basis of their consistency with the principles of self and market discipline. The threat of dilution via conversion of the instrument into common equity creates powerful incentives not just for management to limit excessive risk taking but also for the investors to exert market discipline where they perceive that management is not exercising self-discipline.

In practice, the RBNZ seems to have discounted this benefit on the grounds that that there is too much risk, either by design or by some operational failure, that these instruments might not convert to common equity. They also seem quite concerned with structures that eschew conversion (i.e. loss absorption effected by write-off alone) but they could have just excluded these instruments rather than a blanket ban. Having largely discounted or disregarded the potential benefit, the principles of deliberate conservatism and simplicity dictate their proposed policy position, common equity rules.

This post only scratches the surface of this topic. My key point is that contingent convertible capital instruments potentially add something useful to the bank capital management toolkit compared to relying entirely on common equity. The RBNZ acknowledge the potential upside but ultimately argue that the concerns they identify outweigh the potential benefits. I have reviewed their six concerns in this post but need to do a bit more work to gain comfort that I am not missing something and that my belief in the value of bail-in based capital instruments is justified.

Tony

The Australian Government’s 2014 Financial System Inquiry (FSI) recommended that APRA implement a framework for minimum loss-absorbing and recapitalisation capacity in line with emerging international practice, sufficient to facilitate the orderly resolution of Australian authorised deposit-taking institutions (ADIs) and minimise taxpayer support (Recommendation 3).

In early November, APRA released a discussion paper titled “Increasing the loss absorption capacity of ADIs to support orderly resolution” setting out its response to this recommendation. The paper proposes that selected Australian banks be required to hold more loss absorbing capital. Domestic Systemically Important Banks (DSIBs) are the primary target but, depending partially on how their Recovery and Resolution Planning addresses the concerns APRA has flagged, some other banks will be captured as well.

The primary objectives are to improve financial safety and stability but APRA’s assessment is that competition would also be “Marginally improved” on the basis that “requiring larger ADIs to maintain additional loss absorbency may help mitigate potential funding advantages that flow to larger ADIs“. This assessment may be shaped by the relatively modest impact (5bp) on aggregate funding costs that APRA has estimated or simple regulatory conservatism. I suspect however that APRA is under selling the extent to which the TBTF advantage would be mitigated if not completely eliminated by the added layer of loss absorption proposed. If I am correct, then this proposal would in fact, not only minimise the risk to taxpayers of future banking crises, but also represent an important step forward in placing Australian ADIs on a more level playing field.

APRA offers two reasons:

The need for extra capital might seem counter-intuitive, given that ADI’s are already “unquestionably strong”, but being unquestionably strong is not just about capital, the unstated assumption is that the balance sheet and business model are also sound. The examples that APRA has used to calibrate the degree of total loss absorption capacity could be argued to reflect scenarios in which failures of management and/or regulation have resulted in losses much higher than would be expected in a well-managed banking system dealing with the normal ups and downs of the business cycle.

At the risk of over simplifying, we might think of the first layers of the capital stack (primarily CET1 capital but also Additional Tier 1) being calibrated to the needs of a “good bank” (i.e. well-managed, well-regulated) while the more senior components (Tier 2 capital) represent a reserve to absorb the risk that the good bank turns out to be a “bad bank”.

APRA concludes that ADI’s should be required to hold “private resources” to cope with this contingency. I doubt that conclusion would be contentious but the issue is the form this self-insurance should take. APRA proposes that the additional loss absorption requirement be implemented via an increase in the minimum Prudential Capital Requirement (PCR) applied to the Total Capital Ratio (TCR) that Authorised Deposit-Taking Institutions (ADIs) are required to maintain under Para 23 of APS 110.

“The minimum PCRs that an ADI must maintain at all times are:

(a) a Common Equity Tier 1 Capital ratio of 4.5 per cent;

(b) a Tier 1 Capital ratio of 6.0 per cent; and

(c) a Total Capital ratio of 8.0 per cent.

APRA may determine higher PCRs for an ADI and may change an ADI’s PCRs at any time.”APS 110 Paragraph 23

This means that banks have discretion over what form of capital they use, but APRA expect that banks will use Tier 2 capital that counts towards the Total Capital Ratio as the lowest cost way to meet the requirement. Advocates of the capital structure irrelevance thesis would likely take issue with this part of the proposal. I believe APRA is making the right call (broadly speaking) in supporting more Tier 2 rather than more CET1 capital, but the pros and cons of this debate are a whole post in themselves. The views of both sides are also pretty entrenched so I doubt I will contribute much to that 50 year old debate in this post.

APRA looked at three things when calibrating the size of the additional capital requirement

Based on these inputs, APRA concluded that requiring DSIBs to maintain additional loss absorbing capital of between 4-5 percentage points of RWA would be an appropriate baseline setting to support orderly resolution outcomes. The calibration will be finalised following the conclusion of the consultation on the discussion paper but this baseline requirement looks sufficient to me based on what I learned from being involved in stress testing (for a large Australian bank).

The short answer, I think, is yes. The government needs a robust way to recapitalise banks which does not involve risk to the taxpayer and the only real alternative is to require banks to hold more common equity.

The devil, however, is in the detail. There are a number of practical hurdles to consider in making it operational and these really need to be figured out (to the best of out ability) before the fact rather than being made up on the fly under crisis conditions. The proposal also indirectly raises some conceptual issues with capital structure that are worth understanding.

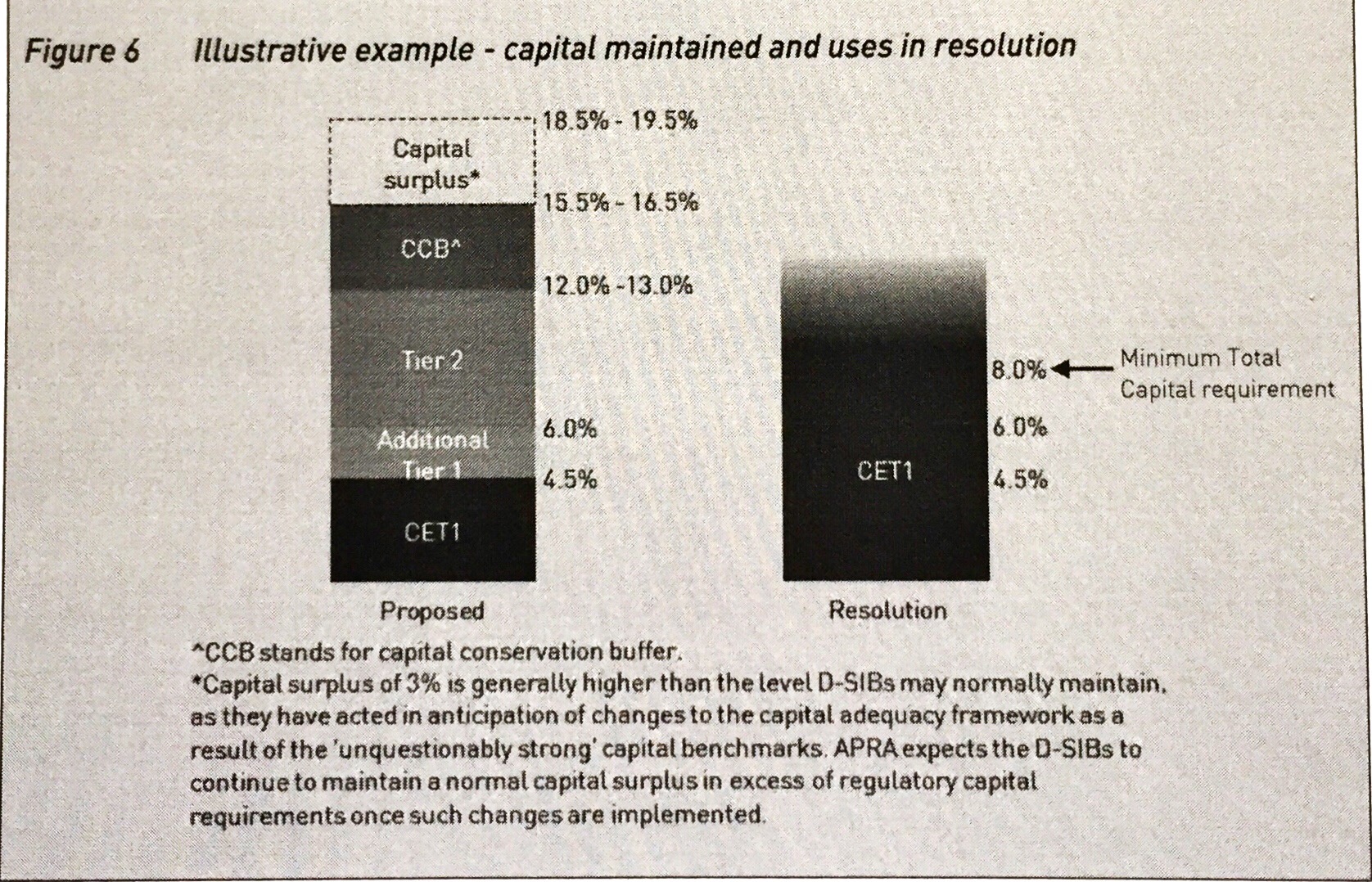

The discussion paper sets out “A hypothetical outcome from resolution action” to explain how an orderly resolution could play out.

“The approximate capital levels the D-SIBs would be expected to maintain following an increase to Total Capital requirements, and a potential outcome following the use of the additional loss absorbency in resolution, are presented in Figure 6. Ultimately, the outcome would depend on the extent of losses.

If the stress event involved losses consistent with the largest of the FSB study (see Figure 2), AT1 and Tier 2 capital instruments would be converted to ordinary shares or written off. After losses have been considered, the remaining capital position would be wholly comprised of CET1 capital. This conversion mechanism is designed to allow for the ADI to be stabilised in resolution and provide scope to continue to operate, and particularly to continue to provide critical functions.”

Source – APRA Discussion Paper (page 24)

What I have set out below draws from APRA’s example while adding detail that hopefully adds some clarity on what should be expected if these scenarios ever play out.

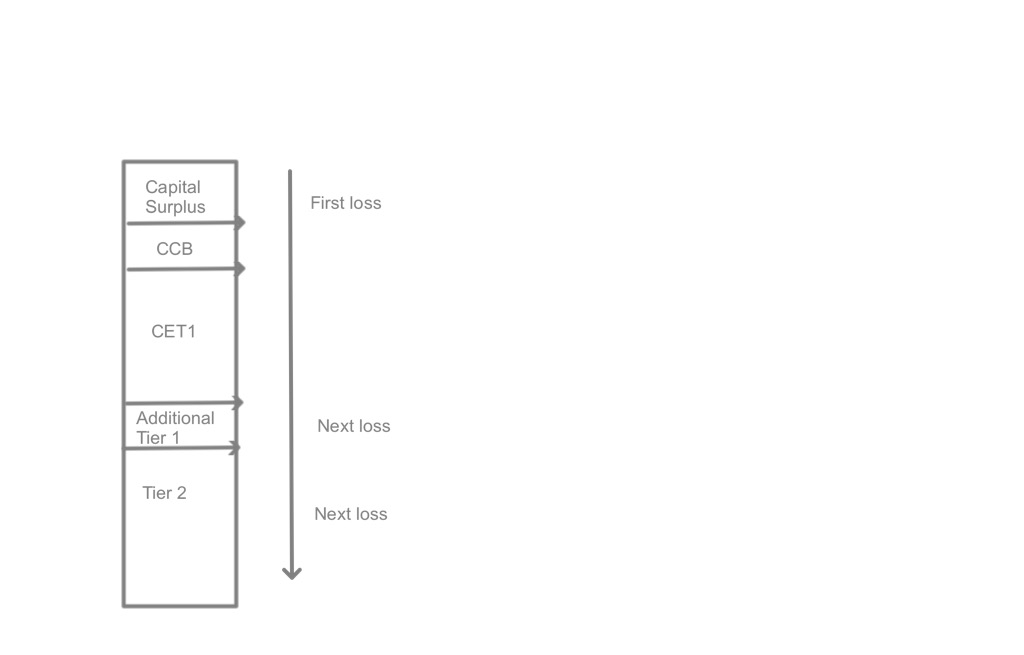

Note that conversion of the AT1 and Tier 2 instruments does not in itself allocate losses to these instruments. The holders receive common equity equivalent to the book value of their instrument which they can sell or hold. The ordinary shareholders effectively bear the loss via the forced dilution of their shareholdings. The main risk to the ATI and Tier 2 holders is that, when they sell the ordinary shares received on conversion, they may not get the same price that which was used to convert their instrument. APRA also imposes a floor on the share price that is used for conversion which may mean that the value of ordinary shares received is less than the face value of the instrument being converted. The reason why ordinary shareholders should be protected in this way under a resolution scenario is not clear.

APRA has requested industry feedback on whether market appetite for Tier 2 capital will be a problem but its preliminary assessment is that:

” … individual ADIs and the industry will have the capacity to implement the changes necessary to comply with the proposals without resulting in unnecessary cost for ADIs or the broader financial system.

Preliminary estimates suggest the total funding cost impact from increasing the D-SIBs’Total Capital requirements would not be greater than five basis points in aggregate based on current spreads. Assuming the D-SIBs meet the increased requirement by increasing the issuance of Tier 2 capital instruments and reducing the issuance of senior unsecured debt, the impact is estimated by observing the relative pricing of the different instruments. The spread difference between senior unsecured debt and Tier 2 capital instruments issued by D- SIBs is around 90 to 140 basis points.”

I have no expert insights on this question beyond a gut feel that the required level of Tier 2 capital cannot be raised without impacting the current spread between Tier 2 capital and senior debt, if at all. The best (only?) commentary I have seen to date is by Chris Joye writing in the AFR (see here and here). The key points I took from his opinion pieces are:

Chris Joye know a lot more about the debt markets than I do, but I don’t think relying on the ability to bail-in senior debt really works. The Discussion Paper refers to APRA’s intention that the “… proposed approach is … designed with the distinctive features of the Australian financial system in mind, recognising the role of the banking system in channelling foreign savings into the economy “ (Page 4). I may be reading too much into the tea leaves, but this could be interpreted as a reference to the desirability of designing a loss absorbing solution which does not adversely impact the senior debt rating that helps anchor the ability of the large banks to borrow foreign savings. My rationale is that the senior debt rating impacts, not only the cost of borrowing, but also the volume of money that foreign savers are willing to entrust with the Australian banking system and APRA specifically cites this factor as shaping their thinking. Although not explicitly stated, it seems to me that APRA is trying to engineer a solution in which the D-SIBs retain the capacity to raise senior funding with a “double A” rating.

Equally importantly, the creation of a new class of Tier 3 instruments seems like a very workable alternative to senior bail-in that would allow the increased loss absorption target to be achieved without impacting the senior debt rating. This will be a key issue to monitor when ADI’s lodge their response to the discussion paper. It also seems likely that the incremental cost of the proposal on overall ADI borrowing costs will be higher than the 5bp that APRA included in the discussion paper. That is not a problem in itself to the extent this reflects the true cost of self insurance against the risk of failure, just something to note when considering the proposal.

APRA has the power to effect increased loss absorption in two ways. One is to convert the more senior elements of the capital stack into common equity but APRA also has the power to write these instruments off. Writing off AT1 and/or T2 capital, effectively represents a transfer of value from the holders of these instruments to ordinary shareholders. That is hard to reconcile with the traditional loss hierarchy that sees common equity take all first losses, with each of the more senior tranches progressively stepping up as the capacity of more junior tranches is exhausted.

Consequently I assume that the default option would always favour conversion over write-off. The only place that I can find any guidance on this question is Attachment J to APS 111 (Capital Adequacy) which states

Para 11. “Where, following a trigger event, conversion of a capital instrument:

(a) is not capable of being undertaken;

(b) is not irrevocable; or

(c) will not result in an immediate and unequivocal increase in Common Equity Tier 1 Capital of the ADI,

the amount of the instrument must immediately and irrevocably be written off in the accounts of the ADI and result in an unequivocal addition to Common Equity Tier 1 Capital.”

That seems to offer AT1 and Tier 2 holders comfort that they won’t be asked to take losses ahead of common shareholders but the drafting of the prudential standard could be clearer if there are other reasons why APRA believe a write-off might be the better resolution strategy. The holders need to understand the risks they are underwriting but ambiguity and uncertainty are to helpful when the banking system is in, or a risk of, a crisis.

The concept of a loss hierarchy describes the sequence under which losses are first absorbed by common equity and then by Additional Tier 1 and Tier 2 capital, if the more junior elements prove insufficient. Understanding the loss hierarchy is I think fundamental to understanding capital structure in general and this proposal in particular:

I recognise that APRA probably tried to simplify this explanation but the graphic example they used (see Figure 6 above) to explain the process shows the Capital Surplus and the CCB (both CET1 capital) sitting on top of the capital stack followed by Tier 2, Additional Tier 1 and finally the minimum CET1 capital. The figure below sets out what I think is a more logical illustration of the capital stack and loss .

Losses initially impact CET1 directly by reducing net tangible assets per share. At the point of a non-viability based conversion event, the losses impact ordinary shareholders via the dilution of their shareholding. AT1 and Tier 2 holders only share in these losses to the extent that they sell the ordinary shares they receive for less than the conversion price (or if the conversion price floor results in them receiving less than the book value of their holding).

Capital irrelevancy M&M purists will no doubt roll their eyes and say surely APRA knows that the overall cost of equity is not impacted by capital structure tricks. The theory being that any saving in the cost of using lower cost instruments, will be offset by increases in the costs (or required return) of more subordinated capital instruments (including equity).

So this school argues you should just hold more CET1 and the cost of the more senior instruments will decline. The practical problem I think is that, the cost of senior debt already reflects the value of the implied support of being too big, or otherwise systemically important, to be allowed to fail. The risk that deposits might be exposed to loss is even more remote partly due to deposit insurance but, possibly more importantly, because they are deeply insulated from risk by the substantial layers of equity and junior ranking liabilities that must be exhausted before assets are insufficient to cover deposit liabilities.

Assuming the market capacity constraint question could be addressed (which I think it can), the solution that APRA has proposed seems to me to give the official family much greater options for dealing with future banking crises without having to call on the taxpayer to underwrite the risk of recapitalising failed or otherwise non-viable banks.

It does not, however, eliminate the need for liquidity support. I know some people argue that this is a distinction without a difference but I disagree. The reality is that banking systems built on mostly illiquid assets will likely face future crises of confidence where the support of the central bank will be necessary to keep the financial wheels of the economy turning.

There are alternative ways to construct a banking system. Mervyn King, for example, has advocated a version of the Chicago Plan under which all bank deposits must be 100% backed by liquid reserves that would be limited to safe assets such as government securities or reserves held with the central bank. Until we decide to go down that path, or something similar, the current system requires the central bank to be the lender of last resort. That support is extremely valuable and is another design feature that sets banks apart from other companies. It is not the same however, as bailing out a bank via a recapitalisation.

I have been sitting on this post for a few weeks while trying to consider the pros and cons. As always, the risk remains that I am missing something. That said, this looks to me like a necessary (and I would argue desirable) enhancement to the Australian financial system that not only underpins its safety and stability but also takes us much closer to a level playing field. Big banks will always have the advantage of sophistication, scale and efficiency that comes with size but any funding cost advantage associated with being too big to fail now looks to be priced into the cost of the additional layers of loss absorption this proposal would require them to put in place.

Tony