FT Alphaville today wrote up some of the highlights they picked up from a report included in the Annual Economic Report published by Bank for International Settlements (BIS).

The highlights I picked up from the Alphaville column included:

- Central Bank Digital Currencies (CBDCs) now seem a matter of when, not if, primarily because the BIS has concluded that they need to get ahead of Big Tech (i.e. Big Tech are pushing ahead with their own versions of digital currency in a number of jurisdictions so central banks need to respond to these initiatives)

- The fact that China is committed to a digital currency with the potential to gain a “first-mover advantage” also seems to be a factor

- The BIS does not however see a CBDC as adding much value if your financial system already has a well functioning, retail fast payments system with all of the safeguards required by know-your-customer regulations

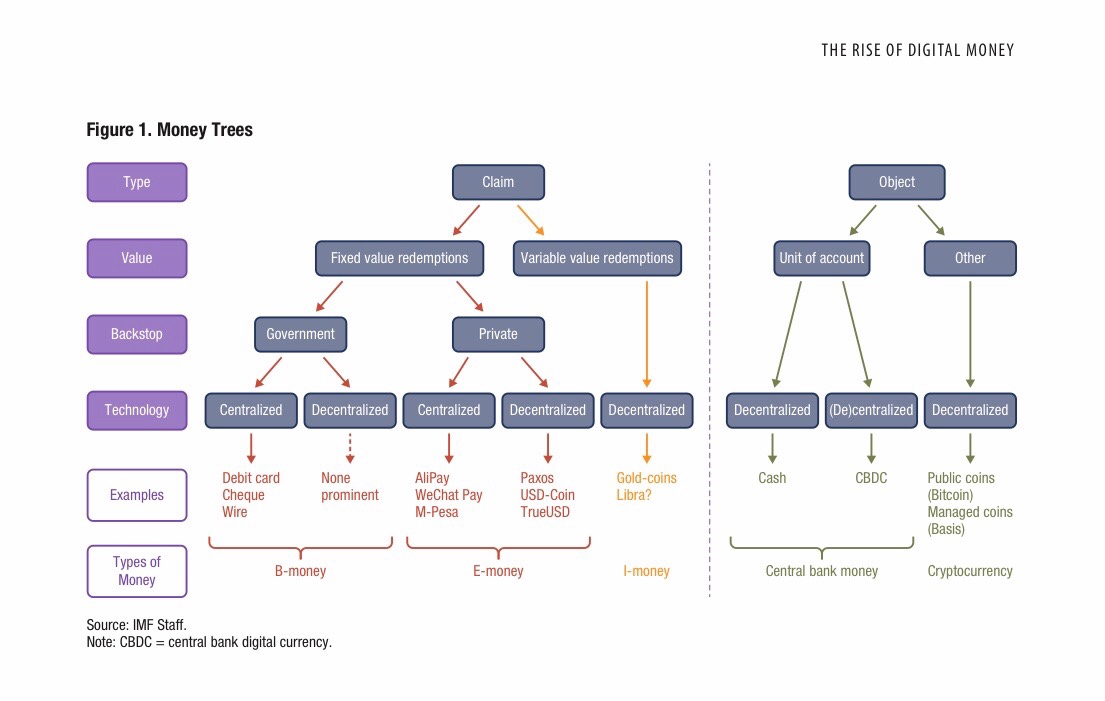

- In terms of design, the BIS seems to be opting for an account based (as opposed to token based) form of digital money

- Two of the larger design issues associated with implementing a CBDC are privacy versus security concerns and the potential for crowding out (i.e. how the new form of digital money impacts financial systems where banks are established as the primary suppliers of digital money).

There is a lot to unpack in the BIS paper but it is worth noting one thing I found immediately curious. In responding to the concerns about privacy versus security, Alphaville noted that “The report … says CBDCs could even have a built-in layer of anonymity for very small inconsequential transactions“.

That might work from an Anti Money Laundering (AML) perspective but it is far from clear to me how you would define “very small inconsequential transactions” in a world where a relatively small number of low value payments can finance child pornography. Westpac Banking Corporation paid a high price for failing to comply with reporting requirements in this regard so it is hard to see how a CBDC could define a threshold that was inconsequential.

Alphaville is of course just one perspective. I am yet to read the BIS paper in full but these are the key takeaways that the BIS author has chosen to highlight:

. Central bank digital currencies (CBDCs) offer in digital form the unique advantages of central bank money: settlement finality, liquidity and integrity. They are an advanced representation of money for the digital economy.

• Digital money should be designed with the public interest in mind. Like the latest generation of instant retail payment systems, retail CBDCs could ensure open payment platforms and a competitive level playing field that is conducive to innovation.

• The ultimate benefits of adopting a new payment technology will depend on the competitive structure of the underlying payment system and data governance arrangements. The same technology that can encourage a virtuous circle of greater access, lower costs and better services might equally induce a vicious circle of data silos, market power and anti-competitive practices. CBDCs and open platforms are the most conducive to a virtuous circle.

• CBDCs built on digital identification could improve cross-border payments, and limit the risks of currency substitution. Multi-CBDC arrangements could surmount the hurdles of sharing digital IDs across borders, but will require international cooperation.

“CBDCs: an opportunity for the monetary system”, BIS Annual Economic Report 2021

Tony – From the Outside