I have posted a couple of time on a Discussion Paper published by The Australian Prudential Regulation Authority (APRA) in late 2020 (“A more flexible and resilient capital framework for ADIs”) setting out how it proposes to wrap up a number of prior consultations on a variety of aspects of ADI (authorised deposit-taking institution) capital reform in Australia (see here, here and here).

This post looks at the changes to mortgage risk weights (RW) outlined in the paper and attempts to explore (with limited information) what practical impact they might have. The short version is:

- In very broad terms, APRA is seeking to assign higher RW to residential mortgages it deems to be relatively more risky but also lower RW for those it considers less risky

- In pursuit of this objective, APRA has proposed two new categories of residential mortgage defined by the loan purpose (i.e. “Owner occupier loans paying principal and interest” and “Other Residential” including loans for investment and all interest only loans upon to 5 years tenor)

- “Standard residential” mortgages see increased sensitivity of RW to Loan Valuation Ratios (LVR) while “Non-Standard residential mortgages face a 100% RW across the board irrespective of their LVR

- Increased sensitivity to LVR is achieved via a simple recalibration of RW in the Standardised approach and via a reduction in the minimum Loss Given Default (LGD) applied in the IRB approach

- The reduced LGD floor also indirectly allows Lenders’ Mortgage Insurance (LMI) to be recognised in the IRB models thereby creating greater alignment with the Standardised approach which directly recognises the value of LMI via a roughly 20% discount in the RW assigned to high LVR loans

- With respect to the impact of RW on competition, APRA argues both that the existing difference between the Standardised and IRB approach is overstated and that the proposed changes will further assist the Standardised ADIs to compete.

APRA is not tinkering at the margins – there are quite substantial adjustments to RWs for both Standardised and IRB ADIs. That is the short version, read on if you want (or need) to dig into the detail.

Improved risk sensitivity cuts both ways

I have looked at “improved risk sensitivity” part of the overall package previously but, with the benefit of hindsight, possibly focussed too much on the expected reduction in aggregate risk weighted assets (RWA) coupled with the expansion of the capital buffers.

It is true that RWA overall are expected to decline – APRA estimated that the overall impact of the proposed revisions would be to reduce average RWAs for IRB ADIs by 10% and by 7% for Standardised ADIs. This obviously translates into higher reported capital ratios which is the impact I initially focussed on. Risk sensitivity however works both ways and a subsequent reading of the paper highlighted (for me at least) the equally important areas in which RW are proposed to increase – residential mortgages in particular.

APRA’s proposed revised approach to residential mortgage risk

APRA was very clear that one of their overall policy objectives is to “further strengthen capital requirements for residential mortgage exposures to reflect risks posed by ADIs’ structural concentration in this asset class“. In pursuit of this objective, APRA is targeting investment and interest only lending in particular but also high LVR lending in general.

In pursuit of these aims, the existing “standard residential mortgage” category is to be further broken down into 1) “Owner Occupied Principal and Interest” loans (OP&I) and 2) “Other Residential”. The “non-standard residential mortgages category (i.e. loans that do not conform to the credit risk origination standards prescribed by APRA) is to be expanded to include interest only loans with a tenor greater than 5 years.

So we get three broad vertical categories of residential mortgage riskiness

| Low Risk | Higher risk | Highest risk |

| Owner Occupied Principal & Interest | – Interest Only (term <5yrs) – Investor mortgage loans – Loans to SME secured by residential property | – Interest Only (term >5yrs) – “Non-standard” mortgages |

Impact on the Standardised ADIs

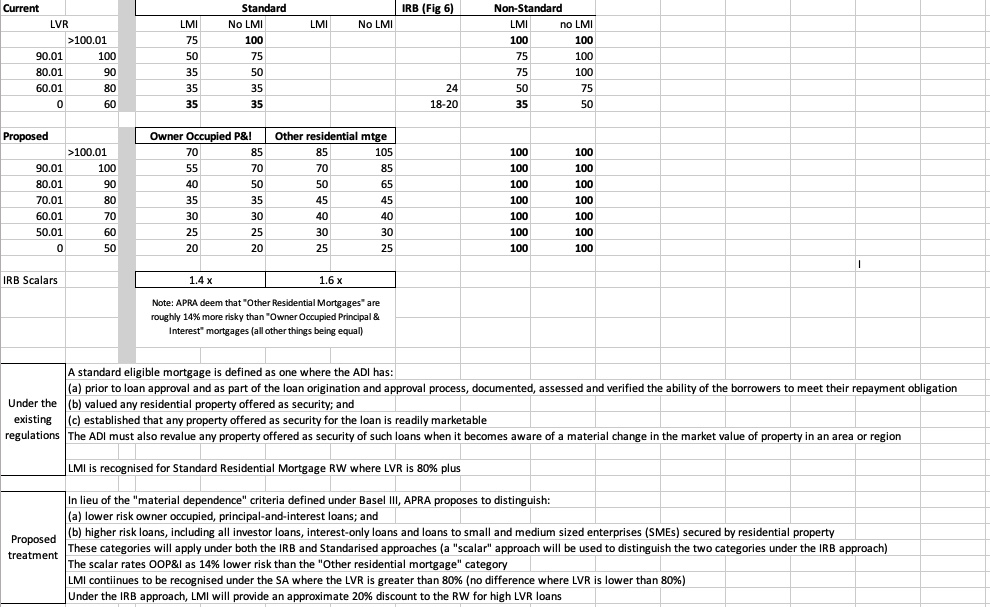

The table below compares the current RWs under the standardised approach (Source: Table 2 of APS 112 – Attachment C) with the indicative RWs APRA has proposed in the December 2020 Discussion Paper (Source: Table 2).

The RW within each of the three categories are being substantially recalibrated – APRA is not tinkering at the edges.

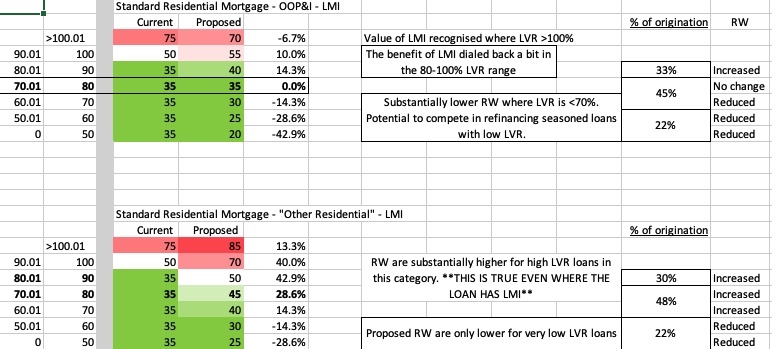

- Increased sensitivity to LVR translates to higher RW applying in the upper LVR range but also reductions in the lower LVR range.

- The increases in the high LVR ranges are particularly marked in the new “Other Residential” category (30-40% increases) but the reductions in the low LVR range are equally material (14-42%) for the OP&I category

- Lender’s Mortgage Insurance (LMI) continues to be recognised at the high end of the LVR range (i.e. 80% plus) but the RW assigned to loans with LMI are higher than is currently applied.

- In case anyone was wondering how APRA really felt about non-standard residential mortgages they receive a 100% RW irrespective of their LVR.

Risk weights under the Internal Ratings Based (IRB) Approach

It is a lot harder to figure out exactly what will happen to IRB RW but the starting point is the two new multipliers being added to the IRB RW formula. The OP&I multiplier adds 40% to RW while the Other Residential category gets a 60% loading. These replace the existing “correlation adjustment” factor that was applied to increase the average IRB RW for residential mortgages to a minimum of 25% as part of the effort to reduce the difference between IRB and Standardised capital requirements.

In aggregate, my guess is that the impacts are roughly neutral in the case of the “Other Residential” loans subject to the 60% loading and a net reduction for the OP&I category. The substitution of flat scalars for the existing correlation adjustment does however create some impacts at the upper and lower ends of the PD scale. Under the correlation approach, my understanding is that low PD exposures increase by proportionately more than the average impact and high PD exposures by less. Under scalar approach, the RW are increased by the same percentage across the PD scale. I am not sure how material the impacts are but mention them for completeness. The flat scalars certainly have the advantage of simplicity and transparency but mostly they establish a RW differential between the two types of standard residential mortgage.

The reduced LGD floor is a significant change because it offers the potential for RW to be halved for exposures that can take the maximum advantage. Consistent with the revised standardised RW, I assume that this will be at the lower end of the LVR range. IRB ADIs will have to work for this benefit however as APRA will first have to approve their LGD models. Some ADIs might be well advanced on this front but as a general rule risk modellers tend to have plenty to do and it is hard to see these models having been a priority while the 20% floor has been in place.

It is also worth noting that the risk differential between OP&I and Other Residential mortgages implied by the multipliers employed in the IRB approach is 14% (i.e. 1.6/1.4) is lower than the 20-30% difference in RW proposed to apply in the Standardised approach. This seems to reflect APRA’s response to comments received (section 4.3 of “Response to Submissions”) that the application of different multipliers could double count risks already captured in the PD and LGD assigned to the two different categories of lending by the IRB risk models.

Impacts, implications and inferences

I can see a couple of implications that follow from these proposed changes

- LGD models start to matter

- The unquestionably strong benchmark is reinforced

- Potential to change the competition equilibrium between the big and small banks

LGD models start to matter

The IRB framework has been a part of the Australian banking system for close to two decades but the 20% LGD Floor has meant that residential mortgage LGD models mostly don’t matter, at least for the purposes of measuring capital adequacy requirements. I am not close enough to the action to know exactly what choices were made in practice but the logical response of credit risk modellers would be to concentrate on models that will make a difference.

APRA’s decision to reduce the LGD floor changes the calculus, IRB ADIs now have an incentive to invest the time and resources required to get new LGD models approved. Loan segments able to take full advantage of the 10% floor will be able to more than offset the impact of the multipliers. The LGD has a linear impact on risk weights so a halving from 20 to 10 percent will see risk weights also halve more than offsetting the 40 to 60% loadings introduced by the multipliers.

Exactly where the cut off lies remains to be seen but it seems reasonable to assume that the increases and decreases proposed in standardised risk weights are a reasonable guide to what we might expect in IRB risk weights; i.e. LGD may start to decline below 20% somewhere around the 70% LVR with the maximum benefit (10% LGD) capping out for LVR of say 50% and below. I have to emphasise that these are just semi educated guesses (hopefully anyway) and I am happy to be corrected by anyone with practical experience in LGD modelling. The main point is that LGD modelling will now have some practical impact so it will be interesting to watch how the IRB ADI respond.

Unquestionably strong is reinforced

On one level, it could be argued that the changes in risk weights don’t matter. ADIs get to report higher capital ratios but nothing really changes in substance. Call me a wide-eyed, risk-capital idealist but I see a different narrative.

First up, we know that residential mortgages are a huge risk concentration for the Australian banks so even small changes can have an impact on their overall risk profiles.

“While an individual residential mortgage loan does not, on its own, pose a systemic risk to the financial system, the accumulation of lending by almost all ADIs in this asset class means that in aggregate the system is exposed to heightened risks”

APRA Discussion Paper, “A more flexible and resilient capiutral framework for ADIs”, 8 December 2020 (page 12)

To my mind, the proposed changes can work in a combination of two ways and both have the potential to make a difference. The decline in residential mortgage risk weights is largely confined to loans originated at low LVRs – less than 70% in the case of “Owner-Occupied Principal and Interest” and less than 60% in the case of “Other Residential”. High LVR risk weights (i.e. 90% plus) are reduced for Owner Occupied Principal and Interest without LMI but my understanding is that these kinds 0f loans are exceptions to the rule, granted to higher quality borrowers and not a large share of the overall exposure. High LVR loans as a rule will face higher risk weights under the proposed changes and materially higher in the case of the “Other Residential” category.

In the low LVR lending, the decline in risk weights seems to be largely offset by higher capital ratio requirements via the increased buffers. In the case of the higher risk, high-LVR lending, the higher capital ratio requirements add to the overall dollar capital requirement.

Competition in residential mortgage lending

APRA has explicitly cited “enhancing competition” as one of their objectives. I don’t have enough hard data to offer any comprehensive assessment of the extent to which competition will be enhanced. The one thing I think worth calling out is the substantial reduction in RW assigned to low LVR loans under the Standardised approach. The table below maps the changes in RW with data APRA publishes quarterly on the amount of loans originated at different LVR bands.

Owner occupiers who have managed to substantially reduce the amount they owe the bank have always been an attractive credit risk; even better if appreciation in the value of their property has further reduced the effective LVR. The proposals reinforce the attraction of this category of borrower. The IRB ADIs will not give up these customers without a fight but the Standardised ADI will have an enhanced capacity t0 compete in this segment via the reduced RW.

At this stage we can only speculate on impacts as the final form of the proposals may evolve further as APRA gets to see the results of the Quantitative Impact Statements that the ADI’s are preparing as part of the consultation process.

Summing up

We are still some way way from seeing the practical impact of these changes and we need to see the extent to which the proposals are refined in response to what APRA learns from the QIS. There does however seem to be potential for the economics of residential mortgage lending to be shaken up so this is a development worth keeping an eye on.

Tony – From the Outside