Interesting post by Marc Rubinstein on the history of clearing houses and Sam Bankman-Fried’s proposal for a new approach.

— Read on www.netinterest.co/p/sbf-and-the-future-of-markets-d79

Interesting post by Marc Rubinstein on the history of clearing houses and Sam Bankman-Fried’s proposal for a new approach.

— Read on www.netinterest.co/p/sbf-and-the-future-of-markets-d79

Another good post from JP Koning’s “Moneyness” blog on the need for DeFi to strike a balance partly between its native potential for transparency, the desire of customers to keep some secrets and the need to meet the same kinds of Know Your Customer – Anti Money Laundering laws that the conventional banking system is required to comply with.

Here is a short extract …

To make their tools palatable for Main Street, DeFi tool makers will have to unwind some of the native anonymity (potentially) afforded by blockchains by collecting and verifying identifying information from users. This way the tools can screen out criminals, assuring legitimate businesses that their clean funds aren’t being tainted by dirty money.

The implication is that DeFi tools will have to become privacy managers, just like old-school banks are. Users will have to trust the tools to be discreet with their personal information, only breaking their privacy when certain conditions are required, such as law enforcement requests.

… and a link to source post.

Tony – From the Outside

JP Koning offers a reminder that, while crypto is disrupting traditional finance, the “no free lunch” rule still applies.

The dangers of stablecoin lending http://jpkoning.blogspot.com/2021/11/the-dangers-of-stablecoin-lending.html

This article in Wired offers a useful summary of how some motivated individuals are attempting to use the transparency of the system to control bad actors.

It is short and worth reading in conjunction with this paper titled “Statement on DeFi Risks, Regulations, and Opportunities Commissioner Caroline A. Crenshaw that sets out a US regulator’s perspective on the question of how DeFi should be regulated. This extract from the paper covers the main thrust of her argument in favours of formal regulation

While DeFi has produced impressive alternative methods of composing, recording, and processing transactions, it has not rewritten all of economics or human nature. Certain truths apply with as much force in DeFi as they do in traditional finance:

– Unless required, there will be projects that do not invest in compliance or adequate internal controls;

– when the potential financial rewards are great enough, some individuals will victimize others, and the likelihood of this occurring tends to increase as the likelihood of getting caught and severity of potential sanctions decrease; and

– absent mandatory disclosure requirements,[10] information asymmetries will likely advantage rich investors and insiders at the expense of the smallest investors and those with the least access to information.

Accordingly, DeFi participants’ current “buyer beware” approach is not an adequate foundation on which to build reimagined financial markets. Without a common set of conduct expectations, and a functional system to enforce those principles, markets tend toward corruption, marked by fraud, self-dealing, cartel-like activity, and information asymmetries. Over time that reduces investor confidence and investor participation.

Conversely, well-regulated markets tend to flourish

“Statement of DeFi Risks, Regulations and Opportunities” by Commissioner Caroline A Crenshaw, The International Journal of Blockchain Law, Vol. 1, Nov. 2021.

Tony – From the Outside

Lately, this blog has pivoted from something I know reasonably well (bank capital adequacy) to things that I don’t – cryptoassets, stablecoins, central bank digital currencies and DeFi. My last post looked at a paper by Nic Cater and Linda Jeng titled “DeFi Protocol Risks: the Paradox of DeFI”. This week I want to flag another useful paper (well at least from my newbie perspective) written by Fabian Schär that was published in the St Louis Fed Review (Second quarter 2021).

I have to confess that I am not yet fully convinced that the DeFI applications developed to date do much more than offer novel ways of trading risk in new forms of securities or crypto assets. That does not mean that the technology will not someday add value to the financial system that will be increasingly called onto support an increasingly digital economy and ultimately the Metaverse.

Schär’s exploration of the risks of DeFI (Section 3) covers very similar ground to the Carter and Jeng paper I flagged above. What I did find useful was Section 2 that lays out the building blocks that DeFi is based on.

Schär concludes …

DeFi has unleashed a wave of innovation. On the one hand, developers are using smart contracts and the decentralized settlement layer to create trustless versions of traditional financial instruments. On the other hand, they are creating entirely new financial instruments that could not be realized without the underlying public blockchain. Atomic swaps, autonomous liquidity pools, decentralized stablecoins, and flash loans are just a few of many examples that show the great potential of this ecosystem.

While this technology has great potential, there are certain risks involved. Smart contracts can have security issues that may allow for unintended usage, and scalability issues limit the number of users. Moreover, the term “decentralized” is deceptive in some cases. Many protocols and applications use external data sources and special admin keys to manage the system, conduct smart contract upgrades, or even perform emergency shutdowns. While this does not necessarily constitute a problem, users should be aware that, in many cases, there is much trust involved. However, if these issues can be solved, DeFi may lead to a paradigm shift in the financial industry and potentially contribute toward a more robust, open, and transparent financial infrastructure.

As noted above, I am not sure that all of the innovations generated by DeFi to date are going to make the world (or at least the financial system) a better place. That said, I am a traditional banker so what would I know. I remain open to the idea (indeed optimistic) that the technologies, applications and concepts being developed under the DeFi framework have the potential to deliver some value. The extent of improvement in conventional banking and finance is sometimes under appreciated but there is still plenty of room for improvement.

Shär’s paper is relatively short (roughly 20 pages) and worth a read if you are new to the topic like me and interested in this area of finance. It also has an extensive list of references that are worth reviewing for leads in areas worth exploring in more depth.

Tony – From the Outside

Nic Carter and Linda Jeng have produced a useful paper titled “DeFi Protocol Risks: the Paradox of DeFi” that explores the risks that DeFi will need to address and navigate if it is to deliver on the promises that they believe it can. There is of course plenty of scepticism about the potential for blockchain and DeFi to change the future of finance (including from me). What makes this paper interesting is that it is written by two people involved in trying to make the systems work as opposed to simply throwing rocks from the sidelines.

Linda Jeng has a regulatory back ground but is currently the Global Head of Policy at Transparent Financial Systems. Nic is a General Partner at a seed-stage venture capital film that invests in blockchain related businesses. The paper they have written will contribute a chapter to a book being edited by Bill Coen (former Secretary General of the Basel Committee on Banking Supervision) and Diane Maurice to be titled “Regtech, Suptech and Beyond: Innovation and Technology in Financial Services” (RiskBooks).

Linda and Nic conceptually bucket DeFi risks into five categories:

… and map out the relationships in this schematic

The paper concludes around the long standing principle firmly entrenched in the traditional financial world – there is “no free lunch”. Risk can be transformed but it is very hard to eliminate completely. Expressed another way, there is an inherent trade off in any system between efficiency and resilience.

Many of the things that make DeFi low cost and innovative also create operational risk and other challenges. Smart contracts sound cool, but when you frame them as “automated, hard-to-intervene contracts” it is easy to see they can also amplify risks. Scalability is identified as an especially hard problem if you are not willing to compromise on the principles that underpinned the original DeFI vision.

The paper is worth a read but if you are time poor then you can also read a short version via this post on Linda Jeng’s blog. Izabella Kaminska (FT Alphaville) also wrote about the paper here.

Tony – From the Outside

As we contemplate new forms of money (both Central Bank Digital Currencies and new forms of private money like stablecoins), JP Koning makes the case that the modern payment systems available in the conventional financial system have improved more than is often appreciated …

The speeding up of modern payments is a great success story. Let me tell you a bit about it.To begin with, central banks and other public clearinghouses have spent the last 15-or-so years blanketing the globe with real-time retail payments systems. Europe has TIPS, UK has Faster Payments, India has IMPS, Sweden has BiR, Singapore FAST. There must be at least thirty or forty of these real-time retail payments system by now.

The speed of these new platforms get passed on to the public by banks and fintechs, which are themselves connected to these core systems.

That is not to say they are perfect but it is helpful to properly understand what has been done already in order to better understand what the new forms truely offer.

You can read his post here ..

http://jpkoning.blogspot.com/2021/07/those-70s-ach-payments.html

Tony – From the Outside

… is the title of an interesting paper by Gary Gorton and Jeffrey Zhang which argues that:

I am not convinced that a central bank digital currency is the solution. I can see a case for greater regulation of stablecoins but you need to be clear about exactly what type of stablecoin requires a policy response. Gorton and Zhang distinguish three categories …

The first includes cryptocurrencies that are not backed by anything, like Bitcoin. We call these “fiat cryptocurrencies.” Their defining feature is that they have no intrinsic value. Second, there are specialized “utility coins,” like the JPMorgan coin that is limited to internal use with large clients. Finally, there are “stablecoins,” which aspire to be used as a form of private money and so are allegedly backed one-for-one with government fiat currency (e.g., U.S. dollars)

I am yet to see a completely satisfactory taxonomy of stablecoins but at a minimum I would break the third category down further to distinguish the ways in which the peg is maintained. The (relatively few?) stablecoins that actually hold high quality USD assets on a 1:1 basis are different from those which hold material amounts of commercial paper in their reserve asset pool and different again from those which employ algorithmic protocols to maintain the peg.

However, you do not necessarily have to agree with their taxonomy, assessments or policy suggestions to get value from the paper – three things I found useful and interesting:

Money is conventionally defined in terms of three properties; a store of value, a unit of account and a medium of exchange. Gorton and Zhang argue that “The property that’s most obvious, yet not explicitly presented, is that money also must satisfy the no-questions-asked (“NQA”) principle, which requires the money be accepted in a transaction without due diligence on its value“. They freely admit that they have borrowed this idea from Bengt Holmstrom though I think he actually uses the term “information insensitive” as opposed to the more colloquial NQA principle.

Previous posts on this blog have looked at both Holmstrom’s paper and other work that Gorton has co-authored on the optimal level of information that different types of bank stakeholders require. If I understood Holmstrom correctly, he seemed to extend his thesis on the value of being able to trade on an “information insensitive” basis to argue that “opacity” in the debt market is something to be embraced rather than eliminated. I struggle with embracing opacity in this way but that in no way diminishes the validity of the distinction he draws between the relative value of information in debt and equity markets and its impact on liquidity.

Gorton and Zhang emphasise the importance of deposit insurance in underwriting confidence in and the liquidity of bank deposits as the primary form of private money. I think that is true in the sense that most bank deposit holders do not understand the mechanics of the preferred claim they have on the assets of the bank they have lent to but it seems to me that over-collateralisation is equally as important in underwriting the economics of bank deposits.

If I have not lost you at this point, you can explore this question further via this link to a post I did titled “Bank deposits – turning unsecured loans to highly leveraged companies into (mostly) risk free assets – an Australian perspective“. From my perspective, the idea that any form of money has to be designed to be “information insensitive” or NQA rings very true.

The paper delves in a reasonable amount of detail into the technicalities of whether stablecoins are economically or legally equivalent to demand deposits and the related question of whether stablecoin issuers might be considered to be banks. The distinction between the economic and the legal status is I think especially useful for understanding how banking regulators might engage with the stablecoin challenge.

The over arching point is that stablecoins that look and function like bank demand deposits should face equivalent levels of regulation. That does not necessarily mean exactly the same set of rules but something functionally equivalent.

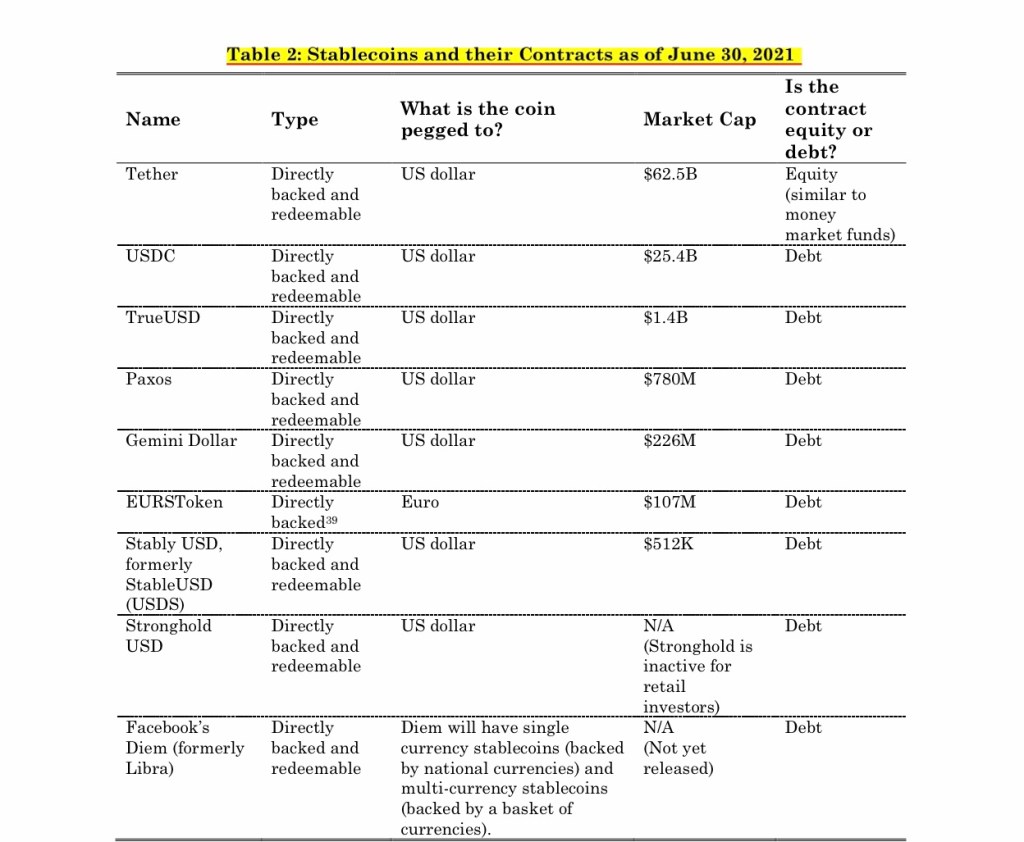

One practical outcome of this analysis that I had not considered previously is that they deem Tether to be based on an “equity contract” relationship with its users whereas the other stablecoins they analyse are “debt contracts” (see below). The link between Tether and a money market fund and the risk of “breaking the buck” has been widely canvassed but I had not previously seen the issue framed in these legal terms.

This technical analysis is summarised in two tables (Table 2: Stablecoins and their Contracts as of June 30, 2021 and Table 3: Stablecoins, Redemptions, and Fiat Money as of June 30. 2021) that offer a useful reference point for understanding the mechanics and details of some of the major stablecoins issued to date. In addition, the appendix to the paper offers links to the sources used in the tables.

It may have been repeated to the point of cliche but the idea that “those who cannot remember the past are condemned to repeat it” (George Santayana generally gets the credit for this but variations are attributed to Edmund Burke and Sir Winston Churchill) resonates strongly with me. The general argument proposed by Gorton and Zhang is that lots of the ideas being tried out in stablecoin design and DeFi are variations on general principles that were similarly employed in the lightly regulated Free Banking Era but found wanting.

Even if you disagree with the conclusions they draw, the general principle of using economic history to explore what can be learned and what mistakes to avoid remains a useful discipline for any practitioner of the dark arts of banking and money creation.

The paper is long (41 pages excluding the Appendix) but I will wrap up this post with an extract that gives you the essence of their argument in their own words.

Tony – From the Outside

Conclusion

The more things change, the more they stay the same. It is still the case that regulation is being outpaced by innovation—thereby creating an uneven playing field—as it is easier and cheaper for more technologically advanced firms to offer similar products and services.

In this case, it is also true that the problems associated with privately produced money are the same as they were one hundred and fifty years ago. We stress three points from our review of history. First, the use of private bank notes was a failure because they did not satisfy the NQA principle. Second, the U.S. government took control of the monetary system under the National Bank Act and subsequent legislation in order to eliminate the private bank note system in favor of a uniform currency—namely, national bank notes. Third, runs on demand deposits only ended with deposit insurance in 1934.

Currently, it does not appear that stablecoins are used as money. But, as stablecoins evolve further, the stablecoin world will look increasingly like an unregulated version of the Free Banking Era—a world of wildcat banking. During the Free Banking Era, private bank monies circulated at time-varying discounts based on geography and the perceived risk of the issuing bank. Stablecoin prices are independent of geography but not independent of the perceived risk of their backing assets. If they succeed in differentiating themselves from fiat cryptocurrencies and become used as money, then they will likely trade at time-varying discounts as well. Policymakers have a couple of ways to address this development, and they better get going.

Grant Williams offers a deep dive into the questions that have dogged Tether via a podcast discussion with two Tether sceptics. In addition (though I am not sure how long this link will be active) he is also offering access to the June edition of his newsletter which includes a detailed account of the case against Tether.

William’s perspective is explicitly Tether sceptical. However, he also includes a long Twitter thread from Jim Bianco attempting (in Bianco’s words) “to pushback on the FUD about USDT”. I am not sure Williams adds anything new to the sceptical view but it is useful to see the counter-narrative offered by Bianco covered in the newsletter. That said, my read of Bianco’s contribution is that it is more a defence of the general promise of a decentralised DeFi system, than it is a defence of Tether itself.

The Tether part of the newsletter is a long read at 25 pages (there is always the podcast if you prefer) but it does offer a comprehensive account of the sceptical position on Tether and a flavour of the counter argument.

Tony – From the Outside

Kudos to “Irony Holder” for a great title to an equally interesting post exploring what went wrong with the IRON stablecoin. My last post “A bank run in CryptoLand” flagged a short summary of the demise of IRON in Matt Levine’s Money Stuff column in Bloomberg and Matt’s latest column put me onto Irony Holder for a more detailed account of what went wrong. I suspect that I will be returning to the stablecoin topic many times before I am done.

One of the challenges in banking and finance is figuring our what is “new and useful” versus what is simply a “new way of repeating past mistakes” and stablecoins offer a rich palette for exploring this question. I remain open to the possibility that stablecoins will produce something more than a useful tool for managing trading in cryptoassets. The potential to make low value international payments cheaper and faster seems like one of the obvious places where the existing financial system could be improved on.

However, it seems equally likely that stablecoin innovation will repeat mistakes of the past so these post mortems are always useful. I recommend reading Irony Holder’s account in full (especially for the code error in the smart contract) but this is what I took away:

I have over four decades of experience in the conventional financial system but I am a “noob” in this space (crypto-DeFi-digital) so the observations above should be read with that caveat in mind. It also important to remember that the issues above do not necessarily extend to other types of stablecoin. My understanding is that the algorithmic approach has not achieved as much traction as fiat and crypto collateralised approaches.

Hopefully you find the links (and summary) useful but also tell me what I am missing.

Tony – From the Outside